A Beginner’s Guide To Estate Planning – Key Concepts You Should Know

Guide your future with effective estate planning, ensuring your assets are managed according to your wishes when the time comes. This process can protect your family, minimize taxes, and avoid lengthy legal battles. As you navigate this necessary journey, understanding key concepts like wills, trusts, and power of attorney will empower you to make informed decisions. In this post, we’ll break down what you need to know, so you can take charge of your estate plan and provide peace of mind for you and your loved ones.

Key Takeaways:

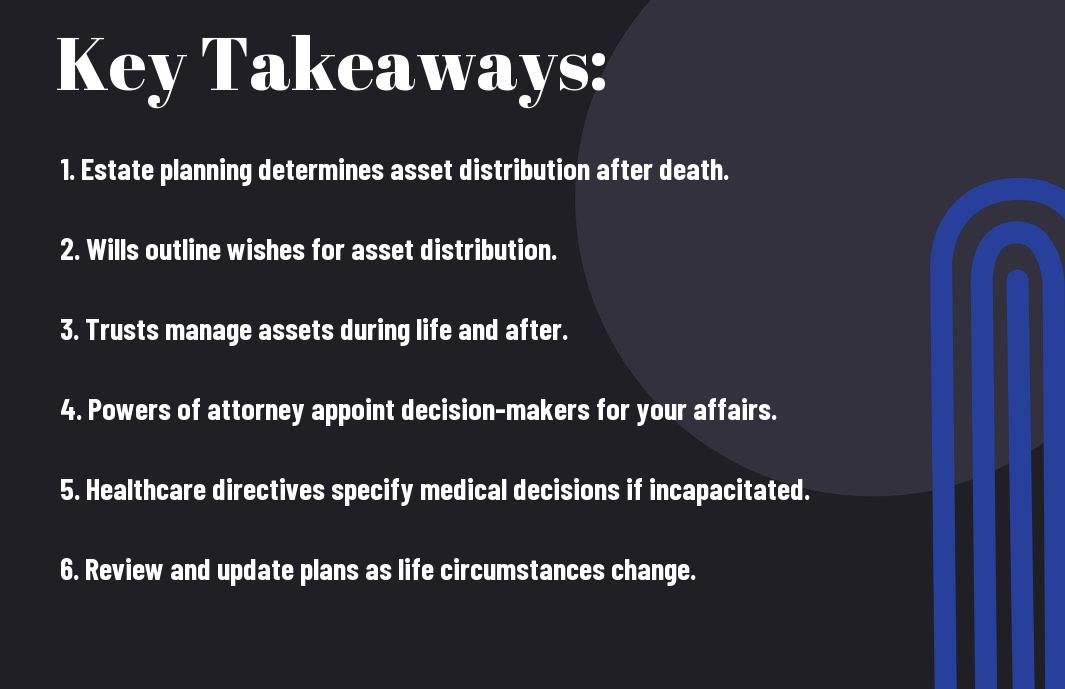

- Estate plan necessarys: An estate plan is vital for organizing your assets and ensuring your wishes are carried out after your passing.

- Wills and trusts: Understanding the differences between a will and a trust is key for effective estate planning; each serves different purposes in asset distribution.

- Beneficiary designations: Regularly updating beneficiary designations on financial accounts can prevent complications and ensure assets go to intended heirs.

- Power of attorney: Assigning a durable power of attorney allows someone to make financial and medical decisions on your behalf if you become incapacitated.

- Tax considerations: Familiarizing yourself with estate taxes can help you strategize your estate plan to minimize tax burdens for your heirs.

Understanding Estate Planning

What is Estate Planning?

Before delving into the specifics, it’s crucial to understand what estate planning entails. Estate planning is the process of arranging for the management and disposal of your assets during your life and after your death. This planning typically involves creating legal documents such as wills, trusts, and powers of attorney, which outline your wishes regarding your finances, healthcare decisions, and the distribution of your property. By engaging in this process, you ensure that your desires are respected when you are no longer able to communicate them.

Importance of Estate Planning

Against popular belief, estate planning is not just for the wealthy or the elderly. Regardless of your financial status, having a well-structured estate plan is an imperative measure for everyone. It grants you the ability to control the distribution of your assets, offers guidance for your loved ones, and can minimize potential conflicts among family members. Additionally, effective estate planning can help to reduce taxes, avoid probate, and ultimately protect your family’s financial future.

This proactive approach not only empowers you but also provides peace of mind for you and your beneficiaries. Engaging in estate planning means that you can avoid leaving your loved ones in a state of confusion or disagreement about your wishes, which can lead to difficult emotions and financial burdens during an already challenging time. By taking these steps now, you can safeguard your assets and provide clear directions on how you would like your affairs to be managed, ensuring that your intentions are honored.

Key Documents in Estate Planning

Some of the most important documents in estate planning include wills and trusts. These key legal instruments help ensure that your wishes regarding asset distribution and management are carried out according to your specifications after you pass away. By understanding these documents, you can better protect your estate and ensure that your loved ones are taken care of, avoiding potential disputes and confusion that may arise in the absence of clear directives.

Wills

Beside being one of the foundational documents in estate planning, a will outlines how you would like your assets distributed upon your death. This legal document allows you to appoint an executor who will be responsible for managing your estate and ensuring that your wishes are fulfilled. Additionally, a will can designate guardians for minor children, making it a vital tool for parents who want to secure the future of their dependents.

Trusts

At the core of many estate planning strategies, trusts serve as powerful tools for protecting and managing your assets during your lifetime and beyond. Unlike a will, a trust can operate during your lifetime, allowing you to transfer assets into the trust for the benefit of your beneficiaries. This not only helps in avoiding probate—the lengthy and often costly legal process that can delay asset distribution—but also provides a level of privacy, as trusts are not made public in the same way that wills are.

Indeed, with trusts, you can stipulate conditions for the distribution of assets, giving you greater control over when and how your beneficiaries receive their inheritance. For example, you can set limitations based on age or milestones, which can help ensure your loved ones use the assets wisely. Furthermore, trusts can also provide significant tax advantages and can be structured to protect assets from creditors, making them an appealing option for many individuals looking to secure their financial legacy for future generations.

Determining Your Assets

Many people overlook the importance of understanding what assets they own when they begin on the estate planning process. Your assets can encompass a variety of items, including real estate, personal property, financial accounts, and even digital assets. By having a clear picture of your assets, you can make informed decisions about how they will be distributed after your passing and ensure that your loved ones are taken care of according to your wishes.

Inventorying Your Assets

Against this backdrop, it is imperative to create a comprehensive inventory of your assets. Start by listing everything you own, from your home and vehicles to valuable collectibles and investments. Be thorough—this involves looking beyond immediate items in your possession and considering items stored away in boxes, your bank accounts, retirement accounts, and any business interests you might have. This inventory will serve as the foundation for your estate planning efforts, helping you decide how to structure your affairs.

Valuing Your Assets

About valuing your assets, it is important to understand not only what you own but also what it’s worth. You may need to conduct a proper valuation for significant assets, such as real estate or business interests. This would involve hiring appraisers or using resources like online valuation tools. Understanding the value of your assets is key to making informed decisions as you craft your estate plan, as it can affect taxes and the specific distributions you intend for your beneficiaries.

Assets may appreciate or depreciate over time, directly impacting their overall value. Goals such as minimizing estate taxes or ensuring fair distribution among heirs can drive your asset valuation. If you have investments, it’s advisable to assess them regularly, as fluctuations in market conditions can influence their worth. You might also need to address any liabilities tied to your assets, such as mortgages or loans, as these factors will ultimately affect your estate’s total value and the financial legacy you intend to leave behind.

Choosing Your Beneficiaries

Keep in mind that selecting your beneficiaries is one of the most vital aspects of estate planning. This process involves assigning individuals or entities who will receive your assets upon your passing. It’s important to understand the different types of beneficiaries to make informed decisions that reflect your wishes. Below is a breakdown of the main categories:

Types of Beneficiaries

| Type of Beneficiary | Description |

|---|---|

| Primary Beneficiaries | Individuals or entities who receive assets directly from your estate. |

| Contingent Beneficiaries | Individuals or entities who will receive assets if the primary beneficiaries are unable to do so. |

| Revocable Beneficiaries | Those you can change or remove from your will or trust at any time. |

| Irrevocable Beneficiaries | Beneficiaries whose designation cannot be changed without their consent. |

| Charitable Beneficiaries | Organizations or charities designated to receive your assets. |

Assume that you have multiple heirs or loved ones with differing needs and circumstances. It’s wise to consider how each type of beneficiary fits into your overall estate plan, ensuring that your intentions are clear and that assets are distributed according to your preferences.

The Importance of Clear Designations

Beneficiaries play a pivotal role in defining how your assets will be managed and distributed in the event of your death. Clear and precise designations help to prevent confusion and potential disputes among heirs. When you spell out your intentions, you ease the burdens on your loved ones during a time of grief, ensuring that your legacy is handled with respect and care. Additionally, a lack of clarity in beneficiary designations can lead to long-lasting family conflicts and litigation.

In fact, when your beneficiary designations align with your overall estate plan, it can make the administration of your estate smoother and more efficient. Updating these designations regularly, especially after significant life events such as marriages or divorces, helps maintain your estate’s integrity. Failing to do so might result in unintended financial hardship for your survivors or charitable organizations you wish to support, which can complicate the distribution of your assets and create unnecessary tensions. It’s important to ensure that your beneficiaries are accurately and thoughtfully designated in your estate planning documents to uphold your wishes and protect your loved ones.

Strategies for Minimizing Taxes

For many individuals, minimizing taxes is an vital part of effective estate planning. By utilizing certain strategies, you can ensure that more of your assets remain within your family or designated beneficiaries, rather than being allocated to tax liabilities. Understanding various tax exemptions and strategies can help you navigate this complex landscape and make informed decisions about your estate. This will not only enhance the financial security of your loved ones but also empower you to leave a legacy according to your wishes.

Gift Tax Exemptions

Along your estate planning journey, gift tax exemptions represent a significant opportunity for you to reduce the size of your taxable estate. The IRS allows you to give a certain amount of money or property each year without incurring gift tax. For 2023, the annual exclusion amount is $17,000 per recipient. This means that you can give up to this amount to multiple individuals per year, effectively lowering your estate’s value while benefiting your loved ones during your lifetime. Additionally, contributions to qualified educational and medical expenses can also be exempt from gift tax, providing further ways to support those you care about.

Estate Tax Strategies

Exemptions and deductions play a significant role in reducing your estate tax liability. By establishing certain strategies, you can take advantage of the federal estate tax exemption, which permits you to transfer assets up to a certain limit (currently $12.92 million for individuals in 2023) without triggering estate taxes. Utilizing vehicles such as trusts, for example, allows you to shift assets out of your estate while still providing for your needs during your lifetime. Furthermore, you might consider charitable contributions, which not only may provide tax benefits but also support causes that matter to you.

Further, it’s important to regularly review these strategies to adapt to any changes in tax law and your personal circumstances. Keeping abreast of any legislative changes, such as alterations to the estate tax exemption limits or gift tax regulations, can help you to make timely adjustments. Collaborating with a knowledgeable estate planner or tax professional can be invaluable in crafting effective strategies that align with your goals to minimize tax implications and secure your estate against potential liabilities, ensuring your loved ones receive the maximum benefit from your hard-earned assets.

Updating Your Estate Plan

Unlike what many people believe, creating an estate plan is not a one-time task. As life evolves, your estate plan must adapt accordingly to reflect your current circumstances and wishes accurately. Regularly updating your estate plan ensures that it remains relevant and effective, safeguarding your loved ones and your assets. By staying proactive with updates, you are taking imperative steps to secure your legacy and ensure your estate will be distributed according to your intentions.

When to Review Your Plan

For most individuals, a complete review of your estate plan every three to five years is advisable, even if there are no immediate changes in your life. This timeframe allows you to reassess your circumstances, address any new regulations or laws, and ensure that your beneficiaries and executors are still appropriate for your current situation. Additionally, it’s a good practice to review your plan whenever there are significant changes in your financial situation or if your attitudes toward your assets evolve.

Life Events that Trigger Updates

When you experience significant life changes, it’s critical to revisit your estate plan promptly. Major events such as marriage, divorce, the birth of a child, or the death of a loved one can have profound implications for your estate distribution and the individuals you choose as your heirs. Additionally, substantial changes in your financial status or the acquisition of new assets should also prompt an update to ensure your estate plan reflects your current wishes.

Understanding the impact of life events is fundamental in ensuring your estate plan stays current. For instance, if you have a new child, you will want to include them as a beneficiary or possibly appoint a guardian, while divorce may necessitate removing an ex-spouse from your will and updating the distribution of your assets. By being mindful of these life changes and their implications for your estate, you can make informed decisions that align your estate plan with your present reality.

To wrap up

On the whole, navigating the landscape of estate planning can seem overwhelming at first, but with the right knowledge and strategies, you can effectively secure your assets and provide for your loved ones. By understanding fundamental concepts such as wills, trusts, and beneficiaries, you are taking proactive steps to ensure your intentions are honored after your passing. It is also imperative to regularly review and update your estate plan to reflect any changes in your life circumstances, such as marriage, divorce, or the birth of a child, to maintain its effectiveness.

Moreover, consulting with professionals in estate planning, such as attorneys or financial advisors, can provide you with personalized guidance tailored to your specific situation. They can help you navigate complex legalities and ensure that your estate plan aligns with your overall financial goals. By investing the time and effort to learn and implement these concepts, you are positioning yourself to make informed decisions about your legacy, which can bring peace of mind for both you and your family.

FAQ

Q: What is estate planning and why is it important?

A: Estate planning involves preparing for the division and management of your assets after your death. It is important because it allows you to ensure that your wishes are carried out regarding your property, healthcare decisions, and guardianship of dependents. Proper estate planning can also help reduce taxes and minimize the financial burden on your loved ones.

Q: What are the key documents involved in estate planning?

A: The primary documents involved in estate planning include a will, which specifies how your assets will be distributed, and a trust, which can help manage your assets during your lifetime and after your passing. Other important documents are a power of attorney, which designates someone to make financial decisions on your behalf if you become incapacitated, and a healthcare proxy or living will, which outlines your healthcare preferences.

Q: How do I choose an executor for my estate?

A: Choosing an executor involves selecting someone you trust to handle your affairs after your death. This individual should be organized, responsible, and capable of managing financial matters. It’s also wise to discuss the role with them beforehand to ensure they are willing to take on the responsibilities and understand your wishes regarding your estate.

Q: Can I amend my estate plan after it is created?

A: Yes, you can amend your estate plan at any time in response to changes in your personal circumstances, such as marriage, divorce, the birth of a child, or changes in financial status. To make changes to your will or trust, it is vital to follow the legal requirements for amendments in your jurisdiction to ensure that the updates are valid.

Q: What are some common misconceptions about estate planning?

A: One common misconception is that estate planning is only for wealthy individuals. In reality, everyone can benefit from estate planning, regardless of their financial situation. Another misconception is that a will can help avoid probate; however, wills typically must go through probate, while certain trusts can help bypass this process. Additionally, some people believe that estate planning is a one-time task, but it should be reviewed and updated regularly as circumstances change.

Ready to protect what you’ve built?

Schedule a no-pressure consultation with Eric Ridley.

Schedule a Consultation