PARENTS & HOMEOWNERS: MY 7-STEP ESTATE PLANNING PROCESS WILL PROTECT YOUR HEIRS

From Creditors, Predators & Bad Choices, And Will Help You Become a (Bigger) Hero to Your Family!

Step by Step Probate Guide: Secure Your Family’s Future

{

“@type”: “Article”,

“author”: {

“url”: “https://ridleylawoffices.com”,

“name”: “Ridley Law Offices”,

“@type”: “Organization”

},

“@context”: “https://schema.org”,

“headline”: “Step by Step Probate Guide: Secure Your Family’s Future”,

“publisher”: {

“url”: “https://ridleylawoffices.com”,

“name”: “Ridley Law Offices”,

“@type”: “Organization”

},

“inLanguage”: “en”,

“articleBody”: “Follow this step by step probate guide to effectively manage your estate, ensuring your family’s future is secured and well-planned.”,

“description”: “Follow this step by step probate guide to effectively manage your estate, ensuring your family’s future is secured and well-planned.”,

“datePublished”: “2025-08-21T01:19:00.214Z”,

“mainEntityOfPage”: {

“@id”: “https://ridleylawoffices.com/step-by-step-probate-guide”,

“@type”: “WebPage”

}

}

Organizing your family’s legacy starts with more than just deciding who gets what. Did you know that missing or incomplete documents are responsible for over 35 percent of probate delays in California? Most people assume probate is just a matter of reading a will and handing out assets, but the reality is a single overlooked form or lost account statement can stall everything for months. Getting this first step right is what makes the difference between a smooth process and a stressful scramble.

Table of Contents

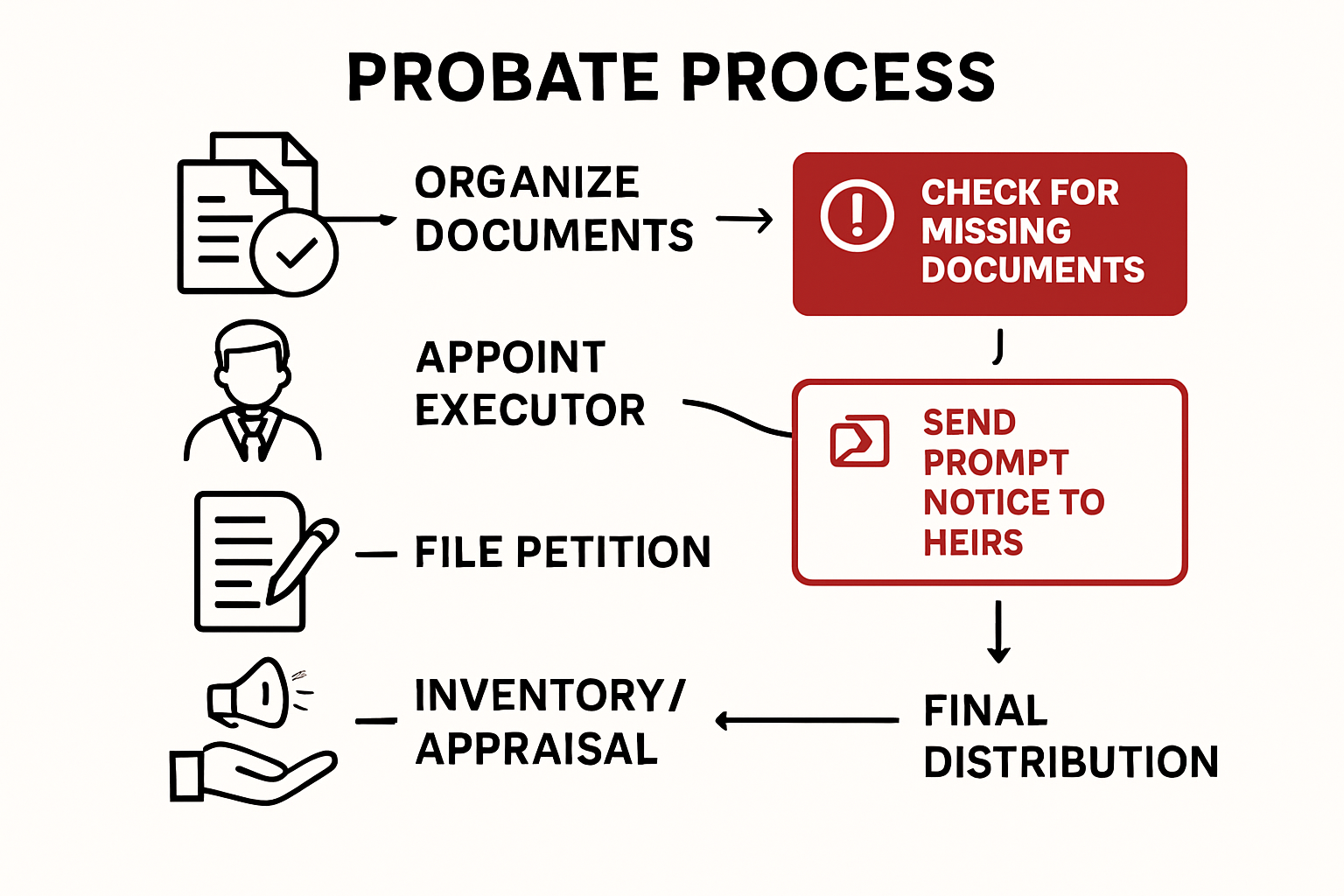

- Step 1: Gather Essential Documents And Information

- Step 2: Identify And Appoint An Executor Or Administrator

- Step 3: File The Probate Petition With The Court

- Step 4: Notify Beneficiaries And Creditors

- Step 5: Inventory And Appraise Estate Assets

- Step 6: Distribute Assets According To The Will

Here is a summary table of the main probate steps, including the goal for each stage and brief notes on what to expect:

| Step | Main Goal | Key Actions/Considerations |

|---|---|---|

| Gather Essential Documents | Organize paperwork | Collect identity, financial, and legal docs |

| Appoint Executor/Administrator | Designate responsible person | Evaluate candidates; confirm willingness |

| File Probate Petition | Begin court proceedings | Complete accurate forms; pay filing fee; submit required docs |

| Notify Beneficiaries & Creditors | Ensure legal transparency | Send written notices; publish announcements; track communications |

| Inventory & Appraise Assets | Provide clear estate valuation | List all assets; get professional appraisals as needed |

| Distribute Assets per Will | Carry out deceased’s wishes | Settle debts; obtain court approval; transfer assets to heirs |

Quick Summary

| Key Point | Explanation |

|---|---|

| 1. Organize Essential Documents | Gather vital documents like birth certificates and financial records to streamline the probate process. |

| 2. Choose a Responsible Executor | Select someone with organizational skills and financial understanding to manage the estate effectively. |

| 3. File the Probate Petition Accurately | Complete and file the probate petition with precise information to avoid delays in court. |

| 4. Notify Beneficiaries and Creditors | Formally inform all beneficiaries and creditors to ensure transparent estate administration. |

| 5. Conduct a Thorough Asset Inventory | Document all assets meticulously for accurate valuation and transparency during distribution. |

Step 1: Gather Essential Documents and Information

Securing your family’s financial future begins with meticulous document organization – a critical first step in the probate process that can significantly streamline estate management. Before diving into complex legal procedures, you need to collect and preserve crucial paperwork that will serve as the foundation of your estate plan.

Start by creating a comprehensive document collection system that includes original copies of key legal and financial records. Your primary focus should be gathering vital personal documents such as birth certificates, marriage licenses, social security cards, and military discharge papers. These foundational documents establish legal identity and familial relationships critical during probate proceedings.

To help you organize everything needed at the start of the probate process, here is a checklist of essential documents and information to gather:

| Document/Information | Type | Purpose/Notes |

|---|---|---|

| Birth certificate | Personal | Establishes legal identity of deceased |

| Marriage license | Personal | Confirms marital status and spouse rights |

| Social Security card | Personal | Required for benefits and official forms |

| Military discharge papers | Personal | Needed for veterans’ benefits and claims |

| Will and codicils | Legal | Outlines distribution wishes |

| Death certificate | Legal | Required for court and financial processes |

| Bank statements | Financial | Confirms account balances and assets |

| Investment/retirement account info | Financial | Documents ownership and value of investments |

| Life insurance policies | Financial | Identifies potential direct payouts |

| Property deeds/vehicle titles | Legal/Financial | Confirms ownership of real estate and vehicles |

| Tax returns (recent years) | Financial | Supports asset/liability verification |

| Debt statements (loans, cards) | Financial | Identifies outstanding liabilities |

Financial documentation represents the next critical category. Compile complete financial records including bank statements, investment account information, retirement account details, life insurance policies, property deeds, vehicle titles, and tax returns from the past several years. Learn how to safely store these important documents to ensure they remain protected and accessible when needed.

Special attention should be given to documenting all assets and liabilities. This means tracking not just tangible property like real estate and vehicles, but also intangible assets such as stocks, bonds, business ownership stakes, and digital assets like cryptocurrency accounts. Create a detailed inventory that lists each asset’s current value, location, and any associated ownership documentation.

Don’t overlook potential complex assets like family businesses, intellectual property rights, or international investments. These require extra documentation and might necessitate professional valuation. Consider working with a financial advisor or estate planning attorney who can help you comprehensively catalog these more nuanced holdings.

As you gather documents, organize them systematically in a secure, fireproof location. Consider creating both physical and digital backups, ensuring that trusted family members or your designated executor knows exactly where to find these critical records. The goal is not just collection, but creating a clear, accessible roadmap that will guide your family through the probate process with minimal confusion and stress.

Step 2: Identify and Appoint an Executor or Administrator

Selecting the right executor or administrator is a pivotal moment in your estate planning journey – this individual will become the critical navigator of your family’s financial legacy after your passing. The executor carries an enormous responsibility of managing complex legal and financial processes, making this choice far more nuanced than simply picking a trusted family member.

When considering potential executors, prioritize individuals with strong organizational skills, financial literacy, and emotional stability. While many people instinctively choose a spouse or eldest child, this isn’t always the wisest strategy. Look for someone who demonstrates meticulous attention to detail, has basic understanding of financial management, and can remain calm during potentially emotional family dynamics. Learn more about selecting a trustworthy executor to ensure your estate is managed effectively.

The ideal executor should possess several key attributes: availability to manage potentially complex legal proceedings, financial acumen to navigate asset distribution, and emotional resilience to handle potential family conflicts. Consider family dynamics carefully – sometimes an impartial third party like a professional fiduciary or trusted attorney might serve your estate more effectively than an emotionally involved family member.

Legal requirements for executors vary by state, but generally they must be over 18, of sound mental capacity, and without significant criminal history. In California, the executor must also be a US resident. If you’re naming a professional executor like an attorney or bank trust officer, ensure they are licensed and have experience managing estate administrations.

Below is a comparison of possible executor choices—family member vs. professional—for managing an estate, so you can evaluate what might work best for your situation:

| Option | Pros | Cons |

|---|---|---|

| Family Member | Knows family dynamics; personal investment; may have lower costs | May lack legal/financial expertise; risk of emotional conflicts |

| Professional Executor | Expertise in law/finance; impartial; avoids conflicts | Additional fees; less personal knowledge of family |

Before finalizing your choice, have an honest conversation with your potential executor. Discuss the responsibilities, potential time commitment, and emotional toll of managing an estate. Confirm they are willing and able to take on this significant responsibility. Additionally, always name alternate executors in case your primary choice becomes unable or unwilling to serve when the time comes.

Once selected, provide your executor with comprehensive documentation about your assets, debts, wishes, and critical contact information. The more organized and transparent you are now, the smoother the eventual probate process will be for your loved ones. Remember, a well-chosen executor can significantly reduce stress and potential conflicts during an already challenging time for your family.

Step 3: File the Probate Petition with the Court

Filing a probate petition marks the official legal commencement of estate administration – a critical transition point where your careful preparation transforms into formal legal action. This step initiates the court’s involvement in managing and distributing your loved one’s assets, transforming your personal documents into an official legal proceeding.

Begin by obtaining the precise probate petition forms required by your local county court. These documents typically include comprehensive details about the deceased, their assets, potential heirs, and the nominated executor. Explore our comprehensive guide to understanding the California probate process to ensure you complete these forms accurately.

Preparing the petition requires meticulous attention to detail. You’ll need to compile original documents including the deceased’s will, death certificate, and a comprehensive inventory of assets. Courts demand precise information, so gather financial statements, property deeds, vehicle titles, and investment account details. Accuracy is paramount – even minor errors can cause significant delays in the probate process.

Once your petition is complete, you must file it with the probate court in the county where the deceased resided. Most courts require multiple copies of the petition, along with appropriate filing fees. These fees vary by jurisdiction but typically range from $200 to $500. Some courts offer fee waivers for individuals with limited financial resources, so inquire about these options if needed.

After filing, the court will schedule a formal hearing and issue a Notice of Petition to all potential heirs and beneficiaries. This notice provides them an opportunity to contest the will or raise objections to the proposed executor. Legally, you must notify these individuals through formal service or certified mail, creating a documented communication trail that protects all parties’ interests.

The court will then review your petition, which can take several weeks to months depending on the complexity of the estate and the court’s current workload. Be prepared for potential requests for additional documentation or clarification. Maintaining organized records and responding promptly to any court inquiries will help streamline this process and demonstrate your commitment to executing the estate efficiently and transparently.

Step 4: Notify Beneficiaries and Creditors

Notifying beneficiaries and creditors represents a critical legal responsibility that transforms your estate administration from private planning to official public process. This step ensures transparency, provides legal protection, and creates a formal mechanism for addressing potential financial claims against the estate.

Beneficiary notification requires precision and comprehensive communication. You must formally contact every individual named in the will, as well as potential legal heirs who might not be explicitly mentioned. Explore our complete guide to understanding probate notifications to ensure you follow all legal requirements. Prepare formal written notices that include key information such as the deceased’s name, date of death, executor’s contact details, and a clear explanation of their potential inheritance or legal interest in the estate.

Creditor notification involves a more complex legal process. You are required to publish a formal notice in a local newspaper, allowing creditors a specific window to file claims against the estate. Additionally, directly notify all known creditors by sending certified letters that outline the deceased’s passing and provide instructions for filing potential claims. Important documentation should include a comprehensive list of outstanding debts, credit card accounts, medical bills, and any loans or financial obligations.

The notification period typically ranges from three to six months, depending on state regulations. During this time, creditors must submit formal claims documenting the exact amount owed. As the executor, you’ll need to carefully review each claim, determining its validity and potential priority. Some claims, like funeral expenses or tax obligations, may take precedence over others.

Careful record-keeping is essential throughout this process. Maintain copies of all notifications, proof of mailings, published notices, and received creditor claims. These documents serve as crucial evidence that you’ve fulfilled your legal responsibilities and provide protection against potential future disputes. Expect this phase to be methodical and sometimes challenging, requiring patience and meticulous attention to detail.

Once the notification period concludes, you’ll have a clear picture of the estate’s financial landscape. This sets the stage for the next critical steps of asset valuation and potential debt settlement, bringing you closer to ultimately distributing remaining assets to beneficiaries.

Step 5: Inventory and Appraise Estate Assets

Inventorying and appraising estate assets represents a complex financial detective work that requires meticulous attention to detail and comprehensive documentation. This critical step transforms abstract ownership into concrete financial valuation, providing a clear snapshot of the deceased’s total economic footprint.

Comprehensive asset identification demands thorough investigation across multiple domains. Begin by gathering documentation for every potential asset – from real estate and vehicles to investment accounts, retirement funds, life insurance policies, and personal property. Learn more about navigating estate asset inventories to ensure you don’t overlook critical financial resources. Professional appraisers or financial experts might be necessary for accurately valuing complex assets like business interests, artwork, or unique collectibles.

Valuation requires precise documentation and strategic approach. You’ll need to determine the fair market value of each asset as of the date of death, which becomes crucial for tax purposes and estate distribution. This means obtaining official appraisals for real estate, getting current statements for financial accounts, and potentially hiring professional appraisers for unique or high-value items. Tax authorities and courts demand exact figures, so precision is paramount.

Financial accounts require special attention. Collect statements from banks, investment firms, retirement accounts, and any digital assets. Some assets might have beneficiary designations that bypass the probate process entirely, so carefully review each account’s specific terms. Pay particular attention to joint accounts, transfer-on-death designations, and any assets with named beneficiaries.

Physical property inventory involves creating a detailed list of significant personal belongings. While not every household item requires individual valuation, high-value items like jewelry, antiques, or specialized equipment should be professionally appraised. Photograph valuable items and maintain detailed descriptions to prevent potential disputes among heirs.

Ultimately, this inventory serves multiple critical functions: it provides a comprehensive financial overview, supports tax filings, guides asset distribution, and creates a transparent record of the estate’s total value. Approach this step with patience, thoroughness, and a commitment to accuracy – your diligence now will smooth the entire probate process and help protect your family’s financial interests.

Step 6: Distribute Assets According to the Will

Asset distribution represents the culmination of the entire probate process – the moment where carefully preserved legal intentions transform into tangible financial transfers. This step requires precision, emotional intelligence, and strict adherence to the deceased’s documented wishes, balancing legal requirements with family dynamics.

Systematic asset distribution begins with comprehensive preparation and court approval. Explore our expert guide to understanding estate settlements to navigate potential complexities. Start by confirming that all financial obligations have been satisfied, including tax payments, outstanding debts, and administrative expenses. Only after these obligations are met can you proceed with distributing remaining assets to designated beneficiaries.

Each asset transfer requires meticulous documentation and potential legal instruments. Real estate might require deed transfers, investment accounts need specific retitling, and personal property distributions demand careful tracking. Some assets may have direct beneficiary designations that bypass probate entirely, while others require formal legal mechanisms to transfer ownership. Executors must maintain transparent records of every transaction, providing receipts and documentation that demonstrate compliance with the will’s instructions.

Emotional intelligence plays a crucial role during asset distribution. Beneficiaries may have conflicting expectations or unresolved family tensions that complicate the process. Clear, compassionate communication becomes as important as legal precision. Schedule individual meetings or family discussions to explain the distribution process, answer questions, and manage potential emotional responses. Some beneficiaries might receive less than anticipated, while others might receive unexpected assets – navigating these moments requires patience and diplomatic skill.

The final stage involves obtaining formal court approval and releasing assets to beneficiaries. This typically requires filing a comprehensive accounting that details all financial transactions, asset valuations, and proposed distributions. The court reviews these documents to ensure legal compliance and fairness. Once approved, you can initiate the final transfers, marking the successful conclusion of your fiduciary responsibilities and helping your loved ones move forward with their inherited resources.

Take the Stress Out of Probate and Secure Your Family’s Legacy

Sorting through probate can be overwhelming. Worrying about missing documents, choosing the right executor, and handling court petitions often leaves families feeling uncertain and unprepared. Without the right guidance, you risk costly delays, stressful disputes, and missed opportunities to protect your loved ones. By learning to organize estate documents, navigate legal forms, and streamline asset distribution, you are taking essential steps to safeguard your family’s future. What if you could get expert help for every step, so nothing is missed and your family’s interests stay protected? Find practical strategies and ongoing support at our dedicated Estate Planning resource hub.

Let the Law Offices of Eric Ridley guide you through the entire probate process with clarity and compassion. From customizing estate plans to assisting with probate administration and estate document management, our California team is your trusted partner.

Take control of your legacy by reaching out today. Start with a no-pressure consultation at ridleylawoffices.com and discover how you can avoid probate headaches and secure peace of mind for your family, now and for generations to come.

Frequently Asked Questions

What are the essential documents needed for the probate process?

To initiate the probate process, you need to gather vital documents such as the deceased’s birth certificate, marriage license, social security card, will, death certificate, and a comprehensive inventory of their assets and liabilities.

How do I choose the right executor for an estate?

When choosing an executor, look for someone with strong organizational skills, financial literacy, and emotional stability. This person should be able to manage legal and financial duties efficiently and be capable of navigating family dynamics without conflict.

What is the process for filing a probate petition?

To file a probate petition, obtain the necessary forms from your local county court. Complete the forms with accurate details about the deceased and their assets, then file them with the probate court along with the required fees and supporting documentation.

How should beneficiaries and creditors be notified during probate?

Beneficiaries should receive formal written notices about their potential inheritance, while creditors need to be notified through published notices in local newspapers and certified letters, allowing them to file claims against the estate.

Recommended

- Preparing for Probate Court in California: Essential Steps for 2025 – Law Office of Eric Ridley

- Understanding Probate Process in California: 2025 Guide for Families and Homeowners – Law Office of Eric Ridley

- Real Estate Probate Sales in California: How Families Secure Their Wealth (2025 Guide) – Law Office of Eric Ridley

- How Probate Works in California: What Families Need to Know in 2025 – Law Office of Eric Ridley