{

“@type”: “Article”,

“author”: {

“url”: “https://ridleylawoffices.com”,

“name”: “Ridley Law”,

“@type”: “Organization”

},

“@context”: “https://schema.org”,

“headline”: “How to Avoid Probate Delays: Secure Your Family’s Future”,

“publisher”: {

“url”: “https://ridleylawoffices.com”,

“name”: “Ridley Law”,

“@type”: “Organization”

},

“inLanguage”: “en”,

“articleBody”: “Learn how to avoid probate delays with a step-by-step process to protect your family’s wealth and ensure a smooth transition of assets.”,

“description”: “Learn how to avoid probate delays with a step-by-step process to protect your family’s wealth and ensure a smooth transition of assets.”,

“datePublished”: “2026-09-05T01:24:51.481Z”,

“mainEntityOfPage”: {

“@id”: “https://ridleylawoffices.com/how-to-avoid-probate-delays”,

“@type”: “WebPage”

}

}

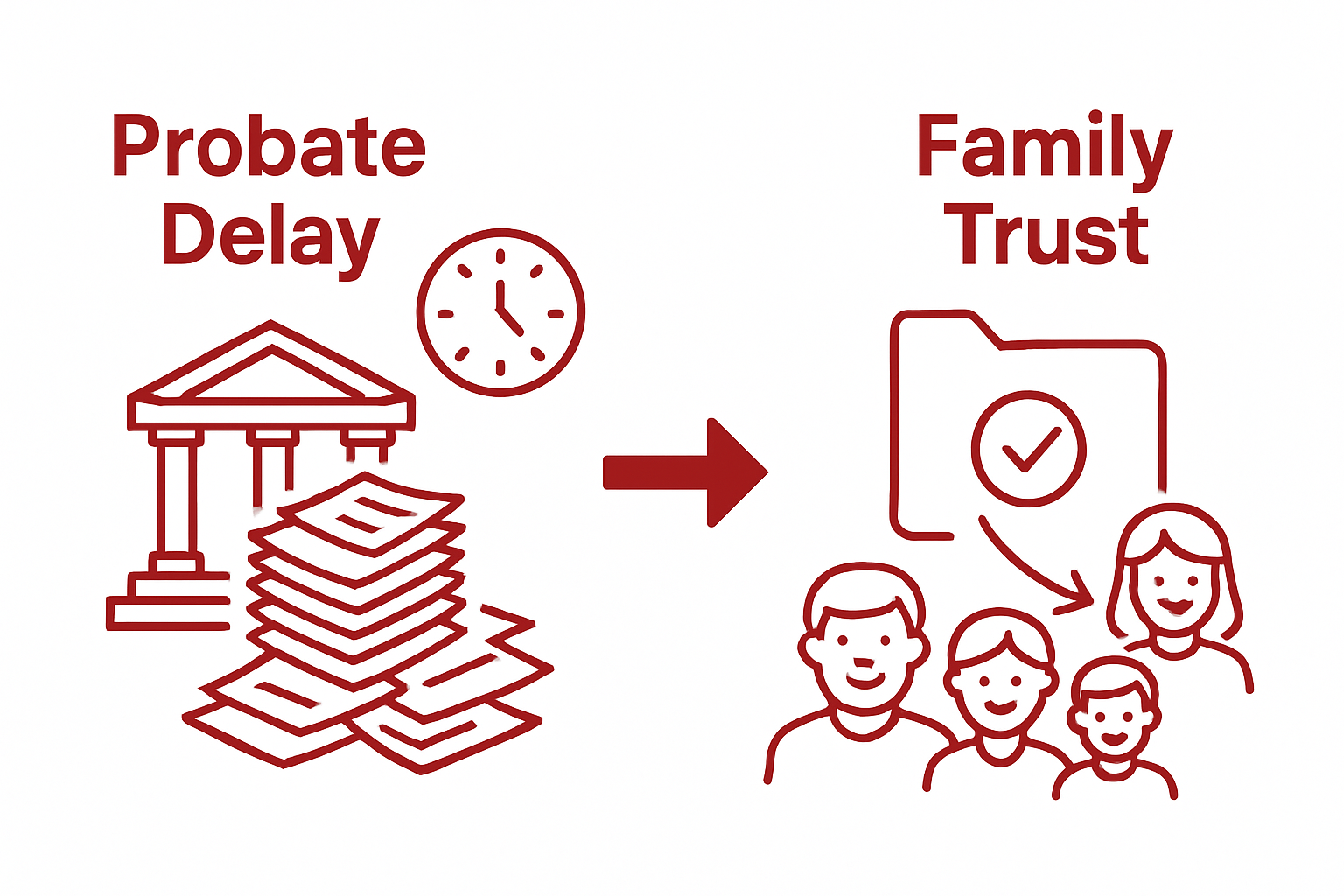

Estate planning often feels overwhelming and complicated but what most people do not realize is probate delays can cost families months or even years in court and drain thousands in fees. Most folks think having a simple will is enough. The real surprise is that the secret to protecting your family and assets from probate nightmares usually comes down to six smart moves that most Americans overlook.

Table of Contents

- Step 1: Assess Your Current Estate Plan

- Step 2: Create A Comprehensive Trust

- Step 3: Designate A Reliable Executor

- Step 4: Fund Your Trust Efficiently

- Step 5: Review And Update Regularly

- Step 6: Communicate With Your Family

Quick Summary

| Key Point | Explanation |

|---|---|

| 1. Review Your Estate Plan Regularly | Conduct a comprehensive assessment every few years or after major life changes to protect your assets and family. |

| 2. Create a Comprehensive Trust | Establishing a trust ensures smooth asset management and bypasses probate, protecting your family’s financial future. |

| 3. Select a Reliable Executor | Choose someone with strong organizational and financial skills to manage your estate effectively during a difficult time. |

| 4. Fund Your Trust Properly | Ensure all assets are transferred into the trust to avoid potential legal complications and probate delays. |

| 5. Communicate Your Estate Plan Clearly | Discuss your estate plan openly with family to prevent misunderstandings and foster a shared understanding of your intentions. |

Step 1: Assess Your Current Estate Plan

Successfully avoiding probate delays starts with a comprehensive review of your existing estate plan. This critical first step helps you understand your current legal and financial landscape, identifying potential vulnerabilities that could trigger complex probate proceedings. Your goal is to create a proactive strategy that protects your family’s future and preserves your hard-earned assets.

Begin by gathering all existing legal documents, including your current will, trust agreements, power of attorney documents, and beneficiary designations. Spread these documents out and conduct a thorough inventory. Look closely at how your assets are currently titled and who is designated to manage them if something happens to you. Many families discover surprising gaps during this review process that could potentially derail their intended estate distribution.

A strategic assessment requires examining your current life circumstances against your existing documentation. Major life events like marriages, divorces, births, deaths, significant financial changes, or relocations can render previous estate plans obsolete. Learn how to update your estate plan to ensure your documents reflect your current wishes and family dynamics.

Careful documentation is key during this assessment. Create a comprehensive spreadsheet or document that includes:

- All financial accounts and their current beneficiary designations

- Real estate and property ownership details

- Life insurance policies

- Retirement accounts

- Outstanding debts and liabilities

- List of digital assets and online accounts

By meticulously documenting your assets and understanding how they are currently structured, you can identify potential probate risks before they become problematic. Your assessment should reveal whether your current estate plan provides smooth, efficient asset transfer or if it contains potential roadblocks that could trigger lengthy and expensive probate proceedings.

Step 2: Create a Comprehensive Trust

Creating a comprehensive trust is your strategic defense against probate delays, transforming how your assets will be managed and transferred after your passing. A well-structured trust acts like a protective shield, ensuring your family avoids the time-consuming and expensive probate process. Unlike a simple will, a trust provides immediate, private asset management that can adapt to your family’s changing needs.

The trust creation process requires careful consideration of your unique family dynamics and financial landscape. Start by identifying all assets you want to transfer, including real estate, investment accounts, business interests, and personal property. Explore the advantages of trust-based estate planning to understand how this approach offers more flexibility and control than traditional estate planning methods.

Deciding on the right type of trust is crucial. A revocable living trust offers the most versatility, allowing you to maintain control of your assets during your lifetime while providing seamless transfer mechanisms. You will need to formally transfer ownership of your assets into the trust, a process called funding. This involves retitling property deeds, changing beneficiary designations, and officially moving financial accounts under the trust’s name. Each asset transfer requires meticulous documentation to ensure legal validity.

Key considerations for trust creation include:

- Selecting a reliable and trustworthy trustee

- Clearly defining distribution instructions

- Establishing precise conditions for asset management

- Creating contingency plans for unexpected scenarios

Work closely with a legal professional who can help you navigate the nuanced details of trust creation. Your goal is a robust, comprehensive document that provides clear guidance, minimizes tax implications, and protects your family’s financial future by avoiding potential probate complications.

Step 3: Designate a Reliable Executor

Selecting the right executor is a critical step in preventing probate delays and ensuring smooth estate administration. Your executor will be responsible for managing complex legal and financial tasks during an emotionally challenging time for your family. This individual becomes the central point of contact for courts, creditors, and beneficiaries, making their selection incredibly important.

The ideal executor combines several key qualities: financial responsibility, organizational skills, emotional stability, and a genuine commitment to your family’s best interests. Often, families default to choosing the oldest child or closest relative, but this approach can lead to potential conflicts or administrative challenges. Learn more about selecting the perfect executor to understand the nuanced considerations beyond familial relationships.

Consider potential executors carefully by evaluating their personal characteristics and practical capabilities. Look for someone who demonstrates strong communication skills, financial literacy, and the ability to remain calm under pressure. Professional executors like attorneys or financial advisors can be excellent alternatives if family members lack the necessary skills or might experience significant emotional strain. Your chosen executor should be someone who can navigate complex legal processes, manage potential family dynamics, and execute your wishes precisely.

Key qualities to assess in a potential executor include:

- Strong organizational and record-keeping abilities

- Financial literacy and basic accounting skills

- Emotional resilience and conflict management capabilities

- Geographical proximity and availability

- Willingness to serve in this critical role

Once you’ve identified a potential executor, have an open conversation about the responsibilities and expectations. Ensure they understand the commitment required and are willing to accept the role. Designate an alternate executor as a backup, providing additional security in case your primary choice becomes unable or unwilling to serve. By carefully selecting and preparing your executor, you significantly reduce the likelihood of probate delays and potential family conflicts.

Step 4: Fund Your Trust Efficiently

Funding your trust is the critical bridge between creating a legal document and actually protecting your assets. Without proper funding, your trust becomes nothing more than an expensive piece of paper, leaving your family vulnerable to the very probate delays you’re working to prevent. This process involves meticulously transferring ownership of your assets into the trust’s name, effectively creating a protective legal structure that bypasses traditional probate proceedings.

Discover the strategic approach to trust funding to ensure comprehensive asset protection. Begin by creating a comprehensive inventory of all assets you want to transfer, including real estate, bank accounts, investment portfolios, retirement accounts, and personal property. Each asset requires specific documentation and transfer procedures, making attention to detail paramount.

The following table summarizes essential types of assets to prioritize when transferring ownership to your trust, along with important notes for each type.

| Asset Type | Examples | Important Notes |

|---|---|---|

| Real Estate | Primary residence, vacation homes, rental properties | Requires new deed listing the trust as owner; formal recording needed |

| Bank Accounts | Checking, savings, CDs | Individual institutions require specific forms for retitling into trust |

| Investment Accounts | Stocks, bonds, mutual funds, brokerage accounts | Ensure all account titles updated; might affect beneficiary designations |

| Retirement Accounts | IRAs, 401(k)s, pensions | Change beneficiary where appropriate; special planning may apply |

| Personal Property | Jewelry, art, collectibles | List high-value items specifically; maintain detailed inventory |

| Business Interests | LLC memberships, partnerships | Amend operating agreements as needed; consult with business attorney |

| Life Insurance Policies | Whole life, term policies | Review beneficiaries; sometimes transfer policy ownership to trust |

Real estate requires particular care during trust funding. You’ll need to draft and record new property deeds that list the trust as the official owner, which typically involves working with a title company or legal professional to ensure proper documentation. Financial accounts demand separate transfer processes, often requiring you to contact individual financial institutions and complete specific paperwork to retitle accounts in the trust’s name.

Key assets to prioritize during trust funding include:

- Primary residence and additional real estate properties

- Checking and savings accounts

- Investment and brokerage accounts

- Retirement accounts with beneficiary designations

- Valuable personal property and collectibles

- Business interests and partnership stakes

Remember that some assets like life insurance policies and retirement accounts with designated beneficiaries might require additional strategic planning. Work closely with a legal professional to ensure each asset is transferred correctly, minimizing potential complications that could inadvertently trigger probate proceedings. Your goal is a seamless, legally sound transfer that provides maximum protection and clarity for your family’s financial future.

Step 5: Review and Update Regularly

Regular estate plan reviews are the maintenance plan that keeps your carefully constructed legal protection functioning smoothly. Your estate plan is not a one-time document but a living strategy that must evolve with your life’s changing circumstances. Neglecting periodic reviews can leave your family vulnerable to unexpected legal complications and potential probate delays.

Understand the critical timing for estate plan updates to ensure your documents remain relevant and effective. Experts recommend conducting a comprehensive review every three years, or immediately after significant life events such as marriages, divorces, births, deaths, substantial financial changes, or major property acquisitions. These moments represent potential trigger points where your existing estate plan might require substantial modifications.

Below is a checklist table summarizing key triggers for reviewing and updating your estate plan, helping you ensure your documents remain current and effective.

| Trigger Event | Description | Suggested Action |

|---|---|---|

| Birth or Adoption | Addition of children or grandchildren to your family | Update documents to include new heirs and adjust asset allocations |

| Marriage or Divorce | Changes in marital status for you or key beneficiaries | Revise estate plan to reflect current relationships and distribution wishes |

| Financial Changes | Significant increase or decrease in personal assets | Reevaluate asset division and update trust funding accordingly |

| Major Asset Transaction | Purchase or sale of important property or investments | Update asset lists and documentation to maintain accurate records |

| Health Changes | Serious illness or decline in capacity | Designate new power of attorney or guardians as needed |

| Retirement or Career Change | Transition to retirement or job change affecting benefits | Review and adjust retirement account designations and beneficiary details |

| Death of Family Member | Passing of a current beneficiary or key participant | Remove or replace names, and adjust allocations in documents |

During your review, meticulously examine every aspect of your estate plan with a critical eye. Assess whether your designated executor still makes sense, if your trust funding remains complete and current, and whether your asset distribution wishes align with your present family dynamics. Consider potential changes in tax laws, shifts in your financial landscape, and emerging family needs that might necessitate adjustments to your existing documentation.

Key triggers for immediate estate plan review include:

- Birth or adoption of children or grandchildren

- Marriage or divorce

- Significant increase or decrease in personal wealth

- Purchase or sale of major assets

- Substantial changes in health status

- Retirement or career transition

Establish a systematic approach to estate plan maintenance by setting calendar reminders, scheduling annual consultations with your estate planning attorney, and maintaining a digital folder with current documentation. Your goal is creating a flexible, responsive estate plan that provides maximum protection and minimal uncertainty for your family’s financial future, effectively neutralizing potential probate complications before they can emerge.

Step 6: Communicate with Your Family

Communicating your estate plan to your family transforms a legal document from a mysterious set of instructions into a shared understanding that can prevent future conflicts and probate delays. Open, honest conversations about your estate plan are not about dictating terms, but creating mutual understanding and preventing potential misunderstandings that could lead to costly legal battles.

Learn strategies for navigating sensitive family discussions to ensure your intentions are clearly understood. The goal is not to create perfect agreement, but to provide transparency that allows your family to understand the reasoning behind your decisions. Choose a neutral, comfortable setting for this conversation, preferably when everyone is calm and not distracted by immediate emotional pressures.

Start by explaining the purpose of your estate plan: protecting your family’s financial future and minimizing potential legal complications. Share the key components of your plan, including who your executor will be, how assets will be distributed, and the reasoning behind specific decisions. Be prepared for potential emotional reactions, and approach the conversation with empathy and patience. Remember that your family members may have different perspectives or unexpected emotional responses to your planning.

Critical elements to discuss during your family meeting include:

- The location of important legal documents

- Contact information for your estate planning attorney

- Names and roles of key individuals in your estate plan

- Basic overview of asset distribution strategy

- Your motivations for specific planning decisions

Consider providing a written summary of key points to help family members process the information. Documentation can serve as a reference point and demonstrate your careful thought process. By proactively communicating your estate plan, you significantly reduce the likelihood of future misunderstandings, potential legal challenges, and the probate delays that can tear families apart during already difficult times.

Protect Your Family from Probate Delays—Start Your Estate Plan Today

Are you worried about probate delays putting your loved ones through uncertainty or stress? If the steps in this article feel overwhelming, you are not alone. People across California realize too late the consequences of incomplete or outdated estate planning. Gaps in trusts, unprepared executors, or missed asset transfers often leave families facing high costs, legal confusion, and even painful conflicts. When it comes to securing your legacy and avoiding probate challenges, you deserve professional guidance and peace of mind. Learn more about how experienced estate planning can make a difference by visiting our Estate Planning & Wills resource page.

Let The Ridley Law be your trusted advisor. Our team will help you ensure your estate plan is current, complete, and built to protect your family’s future. Take the next step NOW and schedule a personal consultation at https://ridleylawoffices.com. Do not let uncertainty put your loved ones at risk—get clarity and control over your estate today.

Frequently Asked Questions

How can I assess my current estate plan to avoid probate delays?

Begin by gathering all existing legal documents such as your will, trust agreements, and power of attorney documents. Conduct a thorough inventory of your assets, their titles, and beneficiary designations to identify any gaps that could lead to probate complications.

What is a comprehensive trust, and how does it prevent probate delays?

A comprehensive trust is a legal arrangement that holds and manages your assets during your lifetime and specifies their distribution after your death. Unlike a will, a trust bypasses probate, allowing for immediate and private asset transfer, thus preventing delays.

What qualities should I look for when designating an executor of my estate?

When choosing an executor, look for qualities such as financial responsibility, organizational skills, emotional stability, and a genuine commitment to your family’s best interests. These traits ensure that your executor can manage the estate efficiently and handle any potential conflicts.

How often should I review and update my estate plan to avoid delays?

It’s recommended to review your estate plan every three years or after significant life events such as marriages, divorces, births, or substantial financial changes. Regular reviews ensure your estate plan remains relevant and effective in avoiding probate complications.

Recommended

Ready to protect what you’ve built?

Schedule a no-pressure consultation with Eric Ridley.

Schedule a Consultation