Life insurance sounds straightforward. Pay your premiums and protect your family if something happens to you. But look closer. Over 60 percent of Americans underestimate how life insurance can shift their entire estate planning strategy. Most people see it as just a safety net. In reality, life insurance can be the most powerful wealth transfer tool you ever use and the surprising linchpin that keeps your family’s financial future intact when everything else gets complicated.

Table of Contents

- Defining Life Insurance And Its Role In Estate Planning

- The Importance Of Life Insurance For Wealth Preservation

- How Life Insurance Works Within An Estate Plan

- Key Considerations For Families Using Life Insurance In Estate Planning

- Real-World Scenarios: Impact Of Life Insurance On Family Wealth

Quick Summary

| Takeaway | Explanation |

|---|---|

| Understand life insurance basics | Learn about term and permanent insurance, which serve different estate planning needs and financial goals. |

| Utilize life insurance for estate liquidity | Life insurance can cover estate taxes and debts, ensuring your heirs receive their inheritance without asset liquidation. |

| Choose beneficiaries wisely | Correct beneficiary designations can streamline the transfer of wealth and influence your overall estate strategy. |

| Leverage tax benefits | Life insurance death benefits are typically tax-free, promoting tax-efficient wealth transfer to your loved ones. |

| Consider policy ownership structure | Ownership affects tax implications; options include individual ownership or using an Irrevocable Life Insurance Trust (ILIT). |

Defining Life Insurance and Its Role in Estate Planning

Life insurance represents a powerful financial instrument that goes far beyond simple monetary protection – it is a strategic tool for comprehensive estate planning. At its core, life insurance provides a financial safety net for your loved ones in the event of your unexpected death, ensuring they remain financially secure during an emotionally challenging time.

Understanding Life Insurance Basics

Life insurance functions as a contract between you and an insurance provider where you pay regular premiums in exchange for a guaranteed lump sum payment to your designated beneficiaries upon your death. Our guide on estate planning fundamentals can help you understand how this mechanism integrates into broader wealth preservation strategies.

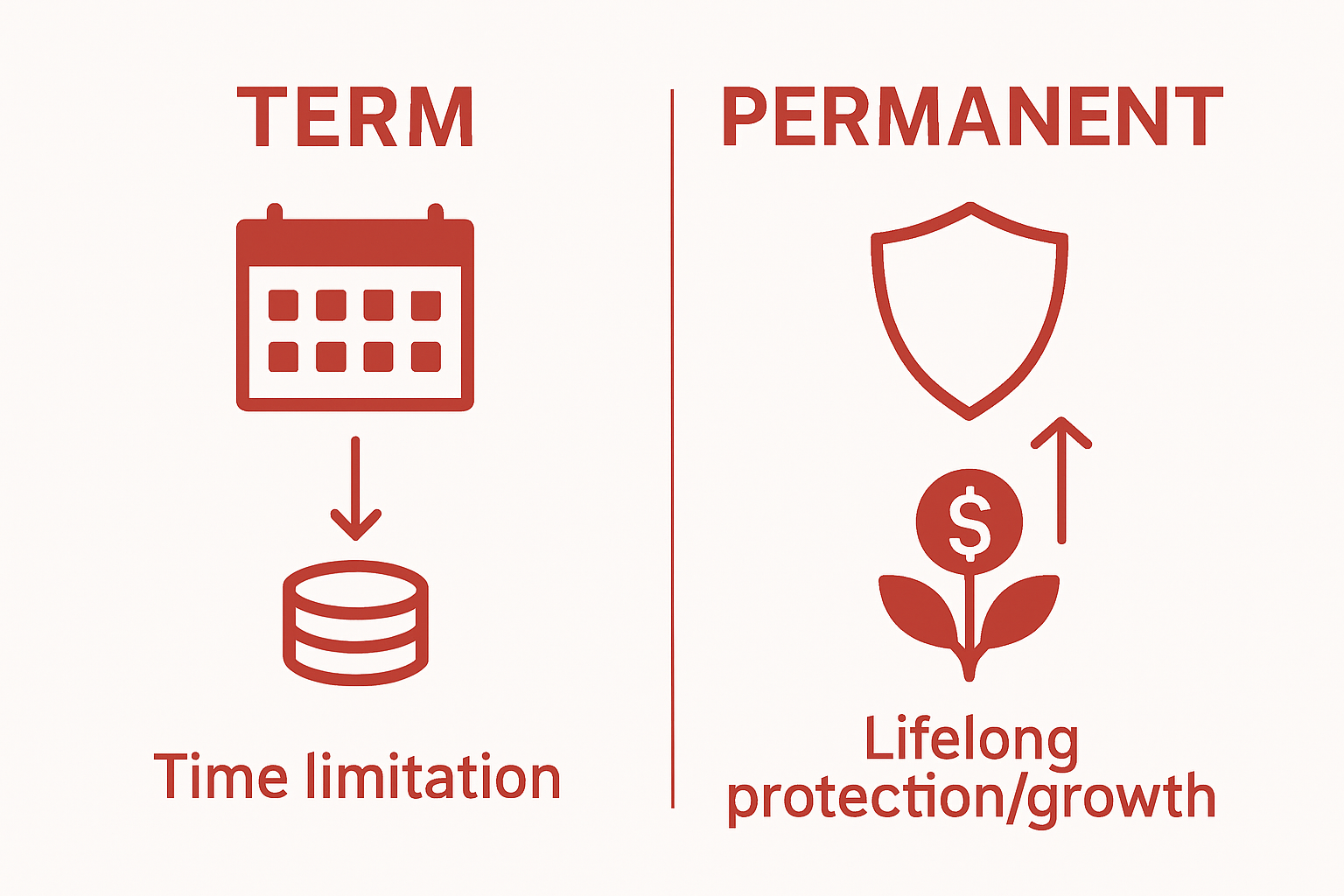

The two primary types of life insurance are term and permanent life insurance:

- Term Life Insurance: Provides coverage for a specific period (10, 20, or 30 years) with lower initial premiums

- Permanent Life Insurance: Offers lifelong coverage with an investment component that builds cash value over time

Strategic Role in Estate Planning

In estate planning, life insurance serves multiple critical functions. According to research from the Congressional report on estate tax policy, life insurance proceeds are generally excluded from gross income and can help maintain estate liquidity. This means the death benefit can cover estate taxes, settlement costs, and provide immediate financial support to your heirs without forcing the sale of valuable assets.

Life insurance also allows you to create an inheritance, even if you have limited savings. By naming specific beneficiaries, you can ensure a precise distribution of wealth that bypasses the often complicated probate process. The death benefit provides a tax-efficient method of transferring wealth to the next generation, helping protect your family’s financial future.

The Importance of Life Insurance for Wealth Preservation

Wealth preservation represents a critical strategy for families seeking to protect their financial legacy across generations. Life insurance emerges as a powerful tool in this process, offering a sophisticated mechanism to safeguard assets and provide financial security beyond an individual’s lifetime.

Financial Protection and Risk Mitigation

Life insurance acts as a strategic financial shield, protecting your family from potential economic vulnerabilities. Learn more about asset protection strategies to understand how life insurance fits into comprehensive wealth management. The death benefit provides a critical safety net that can:

- Replace lost income for dependent family members

- Cover outstanding debts and financial obligations

- Fund educational expenses for children

- Provide immediate liquidity during challenging transition periods

Wealth Transfer and Tax Efficiency

According to research from the Social Security Administration, life insurance serves as an essential method for transferring wealth while minimizing tax implications. The death benefit typically passes to beneficiaries tax-free, allowing families to preserve more of their accumulated assets. This tax-efficient transfer means your hard-earned wealth can continue supporting your family’s financial goals even after your passing.

Moreover, life insurance provides flexibility in estate planning.

The table below summarizes key ways life insurance contributes to both wealth preservation and tax-efficient wealth transfer, as discussed in the article.

| Estate Planning Role | Description | Tax Implication |

|---|---|---|

| Financial Protection | Provides a safety net for dependents and covers debts and obligations | Death benefit usually tax-free |

| Wealth Transfer | Transfers assets efficiently to beneficiaries, often bypassing probate | Typically tax-free; not considered income |

| Estate Liquidity | Supplies immediate funds for estate expenses, preventing forced asset sales | Avoids estate liquidity challenges |

| Business Continuity | Enables partners to buy out shares, protects family business holdings | May limit taxable estate exposure |

| By strategically structuring your policy, you can create a financial legacy that supports your family’s long-term prosperity, ensuring that your wealth continues to provide opportunities and security for future generations. |

How Life Insurance Works Within an Estate Plan

Integrating life insurance into an estate plan requires strategic thinking and careful consideration of your family’s long-term financial needs. This powerful financial instrument serves as more than just a protection mechanism – it becomes a sophisticated tool for comprehensive wealth management and legacy planning.

Structuring Life Insurance for Estate Planning

Learn more about creating a comprehensive estate plan to understand how life insurance fits into your broader financial strategy. When incorporated thoughtfully, life insurance can address multiple estate planning objectives:

- Providing immediate liquidity for estate settlement costs

- Equalizing inheritance among multiple heirs

- Creating a tax-efficient wealth transfer mechanism

- Protecting family businesses from potential financial disruption

Beneficiary Designations and Legal Considerations

According to research from the University of Minnesota Extension, selecting appropriate beneficiaries is crucial in maximizing the effectiveness of life insurance within an estate plan. The beneficiary designation determines how proceeds will be distributed and can significantly impact your overall estate strategy.

Key legal considerations include understanding how life insurance interacts with other estate planning documents like wills and trusts. Properly structured, life insurance can bypass probate, providing a faster and more private method of transferring wealth to your designated beneficiaries. This means your loved ones can access funds quickly during what is often a challenging emotional and financial transition period.

Key Considerations for Families Using Life Insurance in Estate Planning

Life insurance represents a nuanced financial tool that demands careful strategic planning. Families must approach life insurance as more than a simple protection mechanism, understanding its complex role in comprehensive wealth management and long-term financial security.

Understanding Policy Types and Coverage

Learn more about estate planning for young families to contextualize your life insurance needs. Different policy types offer varying benefits and considerations for estate planning:

To help clarify the differences between types of life insurance mentioned in the article, the table below compares their main characteristics and roles in estate planning.

| Type of Life Insurance | Coverage Period | Premiums | Cash Value Component | Estate Planning Benefit |

|---|---|---|---|---|

| Term Life Insurance | 10-30 years (fixed) | Lower | No | Temporary protection; affordable coverage |

| Whole Life Insurance | Lifetime | Higher | Yes | Lifetime security; builds cash value for heirs |

| Universal Life Insurance | Lifetime (flexible) | Flexible | Yes | Flexible premiums; adjustable death benefit |

| Variable Life Insurance | Lifetime | Varies | Yes (market-based) | Cash value can grow based on investments |

- Term Life Insurance: Provides temporary coverage with lower premiums

- Whole Life Insurance: Offers lifetime coverage with cash value accumulation

- Universal Life Insurance: Combines flexibility in premiums and death benefits

- Variable Life Insurance: Allows investment of cash value in market-based subaccounts

Strategic Beneficiary and Ownership Considerations

According to research from the University of Minnesota Extension, selecting appropriate beneficiaries and understanding policy ownership are critical estate planning elements. The ownership structure significantly impacts tax implications and overall estate strategy.

Key considerations include evaluating whether the policy should be owned individually, through a trust, or by another family member. An Irrevocable Life Insurance Trust (ILIT) can potentially remove the policy’s value from your taxable estate, providing additional financial protection for your heirs.

Real-World Scenarios: Impact of Life Insurance on Family Wealth

Life insurance transcends theoretical financial planning, becoming a critical tool for protecting families through practical, real-world financial challenges. Understanding its transformative potential requires examining concrete scenarios where life insurance can fundamentally alter a family’s economic trajectory.

Business Continuity and Inheritance Strategies

Learn more about estate planning after significant life events to comprehend the dynamic nature of financial protection. Life insurance can address complex family and business scenarios such as:

- Enabling surviving business partners to buy out a deceased partner’s share

- Providing immediate funds to prevent forced asset liquidation

- Creating a financial bridge during business transition periods

- Protecting family business investments from unexpected disruptions

Income Replacement and Financial Stability

According to research from Ohio State University, life insurance serves as a critical mechanism for maintaining family financial stability. The death benefit can replace lost income, ensuring that dependents remain financially secure during challenging transitions.

In practical terms, life insurance transforms potential financial vulnerability into a structured economic safety net. For families with primary breadwinners, this means preventing severe economic disruption, maintaining educational opportunities for children, and preserving the family’s standard of living even after the loss of a key income earner.

Secure Your Family’s Future with Simple, Strategic Estate Planning

Are you worried about what will happen to your family or your assets if the unexpected occurs? If you have read about the pitfalls of probate, confusing wealth transfers, or the potential loss of family businesses discussed throughout this article, you are not alone. Many families feel stressed about covering estate taxes, managing inheritance for loved ones, and making sure their life insurance truly protects them.

The right legal guidance makes all the difference. Visit our Estate Planning resources to explore how we help California families integrate life insurance with wills and trusts for lasting financial security.

Take control of your legacy today. Connect with the Ridley Law for personalized advice on estate documents, trust creation, or asset protection. Your future deserves a custom plan that grows with your family. Start your journey with a dedicated advisor who will help you avoid costly mistakes and protect the people you love.

Frequently Asked Questions

What is the role of life insurance in estate planning?

Life insurance serves as a financial safety net, providing immediate funds to cover estate taxes, settlement costs, and ensuring financial stability for loved ones after your passing.

What are the main types of life insurance?

The two primary types are term life insurance, which offers coverage for a specified period, and permanent life insurance, which provides lifelong coverage and includes an investment component that builds cash value over time.

How does life insurance help with wealth transfer?

Life insurance allows for a tax-efficient transfer of wealth to beneficiaries, as the death benefit usually passes tax-free, preserving more of your assets for your heirs without going through probate.

Can life insurance be used to support business continuity?

Yes, life insurance can be used to buy out a deceased partner’s share in a business, providing necessary funds to prevent forced asset liquidation and ensuring business operations continue smoothly.

Recommended

Want a straight read on where you stand?

Talk to Eric. A free 30-minute call, no pitch. He’ll tell you where you’re exposed, what it would cost to fix, and what you can skip.

Talk to Eric