PARENTS & HOMEOWNERS: MY 7-STEP ESTATE PLANNING PROCESS WILL PROTECT YOUR HEIRS

From Creditors, Predators & Bad Choices, And Will Help You Become a (Bigger) Hero to Your Family!

Estate Taxes in California: Complete Expert Guide

{

“@type”: “Article”,

“author”: {

“url”: “https://ridleylawoffices.com”,

“name”: “Ridleylawoffices”,

“@type”: “Organization”

},

“@context”: “https://schema.org”,

“headline”: “Estate Taxes in California: Complete Expert Guide”,

“publisher”: {

“url”: “https://ridleylawoffices.com”,

“name”: “Ridleylawoffices”,

“@type”: “Organization”

},

“inLanguage”: “en”,

“description”: “Estate taxes in California explained. Learn key exemptions, federal vs. state taxes, planning strategies, costs, and critical mistakes to avoid.”,

“datePublished”: “2025-11-11T00:11:19.207Z”

}

More than $5 billion in estate and inheritance taxes are collected by just 17 states and the District of Columbia each year. For California families with significant assets, understanding estate taxes is vital because a single error can expose heirs to unexpected tax bills. Knowing how federal regulations and shifting exemptions affect your estate means you can protect your legacy, sidestep costly surprises, and make smarter decisions about your family’s future.

Table of Contents

- Defining Estate Taxes In California

- Federal Versus State Estate Tax Rules

- Key Exemptions And Exclusions Explained

- Estate Planning Strategies To Minimize Taxes

- Common Pitfalls And Costly Mistakes

Key Takeaways

| Point | Details |

|---|---|

| Federal Estate Tax Exemption | Understanding federal exemption thresholds is crucial, as the exemption amount is set to decrease in 2026, potentially increasing tax liabilities for many families. |

| Strategic Planning | High-net-worth individuals should employ advanced estate planning strategies, like irrevocable trusts and lifetime gifting, to minimize tax exposure and protect assets. |

| Regular Updates | Families must regularly update estate planning documents to reflect significant life changes and avoid costly mistakes related to outdated information. |

| Professional Guidance | Relying on professional estate planning expertise is essential to navigate complex regulations and prevent financial pitfalls. |

Defining Estate Taxes in California

Estate taxes represent a critical financial consideration for families and individuals with significant assets in California. According to Cornell Law, estate tax is a federal tax imposed on the transfer of property at death, calculated on the decedent’s entire taxable estate before distribution to heirs.

Estate taxes are essentially the government’s method of collecting a final tax payment on the total value of a deceased person’s assets. In California, this process is nuanced and complex, involving both federal and state regulations. The tax applies to the total net value of all property, investments, cash, securities, real estate, and other assets owned at the time of death.

California has some unique characteristics when it comes to estate taxation. While the state does not currently impose its own separate estate tax, residents are still subject to potential federal estate tax obligations. For high net worth individuals with estates exceeding the federal exemption threshold, this can represent a significant financial consideration. Learn more about minimizing estate taxes in California to better understand your potential tax liability.

Key components of estate taxes in California include:

- Total asset valuation at time of death

- Federal estate tax exemption thresholds

- Potential tax rates for estates exceeding exemption limits

- Strategies for estate tax planning and reduction

Navigating estate taxes requires careful planning and professional guidance to protect your family’s financial legacy and minimize potential tax burdens.

Federal Versus State Estate Tax Rules

Understanding the complex landscape of estate taxes requires distinguishing between federal and state regulations. Center on Budget and Policy Priorities reports that as of June 2021, only 17 states and the District of Columbia levy an estate or inheritance tax, generating approximately $5 billion annually. This means the majority of states do not impose additional estate taxes beyond federal requirements.

Federal estate tax represents a significant financial consideration for high-net-worth individuals. Currently, the federal government imposes a tax on estates exceeding a specific exemption threshold, which changes periodically. Estates valued below this threshold are not subject to federal estate taxation, providing substantial protection for most middle-class families. California estate tax planning becomes crucial for those approaching or exceeding these federal limits.

The relationship between federal and state estate taxes is intricate and interdependent. According to research from the Center on Budget and Policy Priorities, repealing the federal estate tax could significantly impact states’ ability to maintain their own estate tax structures. Most states currently rely entirely or substantially on the federal tax as the basis for their estate tax calculations.

Key differences between federal and state estate tax rules include:

- Federal exemption thresholds

- State-specific tax rates

- Variations in asset valuation methods

- Potential additional state-level inheritance taxes

Navigating these complex regulations requires careful planning and professional guidance to minimize tax liabilities and protect your family’s financial legacy.

Key Exemptions and Exclusions Explained

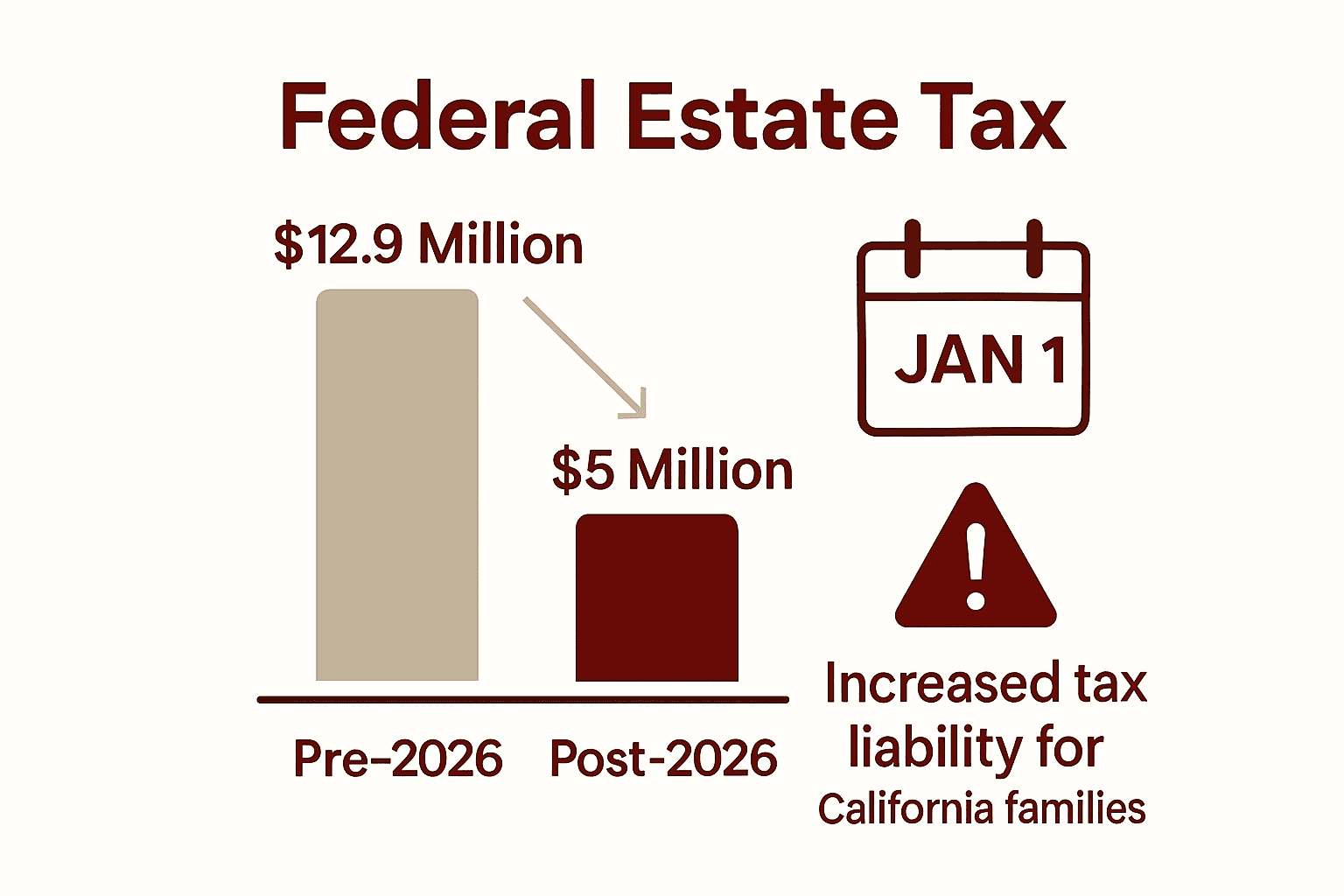

Understanding estate tax exemptions is critical for protecting your family’s financial legacy. The federal government provides substantial protections through estate tax exemptions that shield a significant portion of an estate’s value from taxation. KDA Inc. warns that a critical change is approaching: the federal estate tax exemption is scheduled to drop by half starting January 1, 2026, which could dramatically increase tax liability for many families.

Key estate tax exemptions and exclusions provide important financial safeguards for individuals and families. The primary federal exemption allows a substantial amount of an estate to pass tax-free to heirs. Currently, this exemption is quite generous, protecting millions of dollars from federal taxation. How taxes affect your estate plan becomes crucial as families approach and navigate these complex exemption thresholds.

For California residents, understanding these exemptions requires careful planning. While California does not impose its own state-level estate tax, federal exemptions still play a critical role in estate planning. The exemption amount is adjusted annually for inflation, and strategic planning can help maximize the protection of your assets. Couples can potentially double their exemption through careful estate planning strategies, allowing for even greater asset protection.

Critical exemptions and exclusions include:

- Unified Federal Estate and Gift Tax Exemption

- Marital deduction for transfers between spouses

- Charitable donation exclusions

- Annual gift tax exclusion

- Lifetime gift tax exemption

Navigating these exemptions requires sophisticated planning and professional guidance to ensure your family’s financial security and minimize potential tax burdens.

Estate Planning Strategies to Minimize Taxes

Estate tax minimization requires sophisticated and proactive planning for high-net-worth families. KDA Inc. recommends that high-net-worth individuals strategically explore methods such as trusts, gifting, and entity planning to shield assets from potentially significant federal estate tax liabilities.

One of the most powerful strategies involves creating irrevocable trusts, which can remove assets from your taxable estate while still providing financial benefits to your beneficiaries. Lifetime gifting emerges as another critical approach, allowing individuals to transfer wealth to heirs gradually and reduce their overall estate’s taxable value. How to minimize taxes through estate planning becomes crucial for families seeking to preserve their financial legacy while minimizing tax exposure.

Advanced estate planning techniques offer multiple layers of protection. Sophisticated strategies like family limited partnerships, charitable remainder trusts, and generation-skipping trust structures can provide significant tax advantages. These approaches not only minimize tax liability but also offer enhanced asset protection and controlled wealth transfer mechanisms. The key is creating a comprehensive plan that adapts to changing tax laws and family dynamics.

Key tax minimization strategies include:

- Establishing irrevocable life insurance trusts

- Implementing annual gift tax exclusion strategies

- Creating family limited partnerships

- Utilizing charitable donation techniques

- Establishing generation-skipping trusts

Successful estate tax planning requires a holistic approach that balances tax efficiency with your family’s unique financial goals and personal values.

Common Pitfalls and Costly Mistakes

Estate tax planning is fraught with potential errors that can significantly impact your family’s financial future. KDA Inc. highlights a critical misconception: assuming the absence of a state estate tax in California eliminates the need for comprehensive planning. This dangerous assumption overlooks the substantial impact of federal estate taxes, which can devastate unprepared families.

One of the most prevalent mistakes is failing to regularly update estate planning documents. Life changes such as marriages, divorces, births, deaths, and significant financial shifts can render existing plans obsolete. Common mistakes to avoid in estate planning becomes crucial for families seeking to maintain the relevance and effectiveness of their estate strategies. Outdated beneficiary designations, overlooked asset transfers, and incomplete documentation can create unexpected legal and financial complications.

Do-it-yourself estate planning represents another significant risk. Many individuals mistakenly believe they can create comprehensive estate plans without professional guidance. This approach often leads to critical oversights, including improper trust formations, inadequate tax strategies, and insufficient asset protection mechanisms. Complex legal requirements and ever-changing tax regulations demand expert navigation to avoid potentially catastrophic financial consequences.

Critical estate planning mistakes include:

- Neglecting to create a comprehensive estate plan

- Failing to update documents after major life events

- Attempting DIY estate planning without professional guidance

- Overlooking potential federal tax liabilities

- Inadequate asset protection strategies

- Improper beneficiary designations

Protecting your family’s financial legacy requires proactive, professional estate planning that anticipates potential challenges and adapts to changing circumstances.

Secure Your Family’s Future with Expert Estate Planning in California

Facing the complexities of estate taxes in California can feel overwhelming. The challenges of navigating federal exemption thresholds, protecting assets, and understanding critical strategies like irrevocable trusts and lifetime gifting demand clear guidance. You want to safeguard your family’s legacy and minimize the heavy tax burdens that can arise without proper planning. Our team understands these concerns and is here to help you create a customized plan that works for your unique financial situation.

Explore comprehensive solutions tailored to your needs through our Estate Planning – Law Office of Eric Ridley services.

Don’t wait until tax laws change or an unexpected event complicates your estate. Take control today by partnering with experienced estate planning professionals who prioritize your peace of mind and financial security. Visit us now at https://ridleylawoffices.com or learn how trusts and wills can protect your assets with our Wills & Trusts – Law Office of Eric Ridley. Secure your future before it’s too late.

Frequently Asked Questions

What are estate taxes in California?

Estate taxes are taxes imposed on the total value of a deceased person’s assets before distribution to heirs. In California, while there is no state estate tax, residents may still be liable for federal estate taxes if their estates exceed federal exemption thresholds.

How is the federal estate tax exemption determined?

The federal estate tax exemption is a specific amount of an estate’s value that can pass to heirs without incurring tax. This exemption amount is adjusted annually for inflation and can change, with a significant reduction expected in 2026.

What strategies can help minimize estate taxes?

Effective strategies for minimizing estate taxes include creating irrevocable trusts, utilizing lifetime gifting, establishing family limited partnerships, and charitable donation techniques. Each of these methods can lower the taxable value of an estate and protect family assets.

What are common mistakes in estate tax planning?

Common pitfalls include failing to update estate planning documents after major life changes, neglecting to create a comprehensive estate plan, and attempting to handle estate planning without professional guidance. These errors can lead to unintended tax liabilities and complications for heirs.

Recommended

- The Impact of California Laws on Estate Planning – Law Office of Eric Ridley

- California Estate Tax Planning 2025: Protecting Your Family’s Wealth – Law Office of Eric Ridley

- How to Minimize Estate Taxes in California – Law Office of Eric Ridley

- California Probate Process Explained: 2025 Guide for Families and Homeowners – Law Office of Eric Ridley