PARENTS & HOMEOWNERS: MY 7-STEP ESTATE PLANNING PROCESS WILL PROTECT YOUR HEIRS

From Creditors, Predators & Bad Choices, And Will Help You Become a (Bigger) Hero to Your Family!

Revocable vs Irrevocable Trust: Smart Estate Planning 2025

Estate planning gets a lot of buzz, but most people do not realize the true power hidden in the right kind of trust. Believe it or not, irrevocable trusts can slice your estate taxes and shield assets in ways revocable trusts simply cannot. Yet, the flexibility and personal control offered by a revocable trust often lead families to overlook the crucial protections they are giving up. What if the strategy you think is safest is actually the one putting your family’s wealth at the most risk?

Table of Contents

- Key Differences Between Revocable And Irrevocable Trusts

- Which Trust Is Right For Your California Family?

- Protecting Children And Wealth From Probate And Taxes

- Real-Life Scenarios: Avoiding Common Estate Planning Mistakes

Quick Summary

| Takeaway | Explanation |

|---|---|

| Control and Flexibility | Revocable trusts offer maximum flexibility, allowing the grantor to modify or dissolve the trust at any time, making them ideal for families with changing needs. |

| Tax Benefits of Irrevocable Trusts | Irrevocable trusts remove assets from the grantor’s taxable estate, providing significant tax planning opportunities that can protect wealth for future generations. |

| Asset Protection | Irrevocable trusts offer stronger asset protection against creditors and legal claims, while revocable trusts provide minimal safeguards, making trust choice crucial for high-risk professionals. |

| Regular Updates are Crucial | Trust documents should be reviewed every three to five years or after major life changes to ensure they align with current family dynamics and financial situations, preventing costly errors. |

| Strategic Estate Planning | A comprehensive trust strategy often involves using both revocable and irrevocable trusts, tailored to individual family circumstances to minimize taxes and ensure effective asset distribution. |

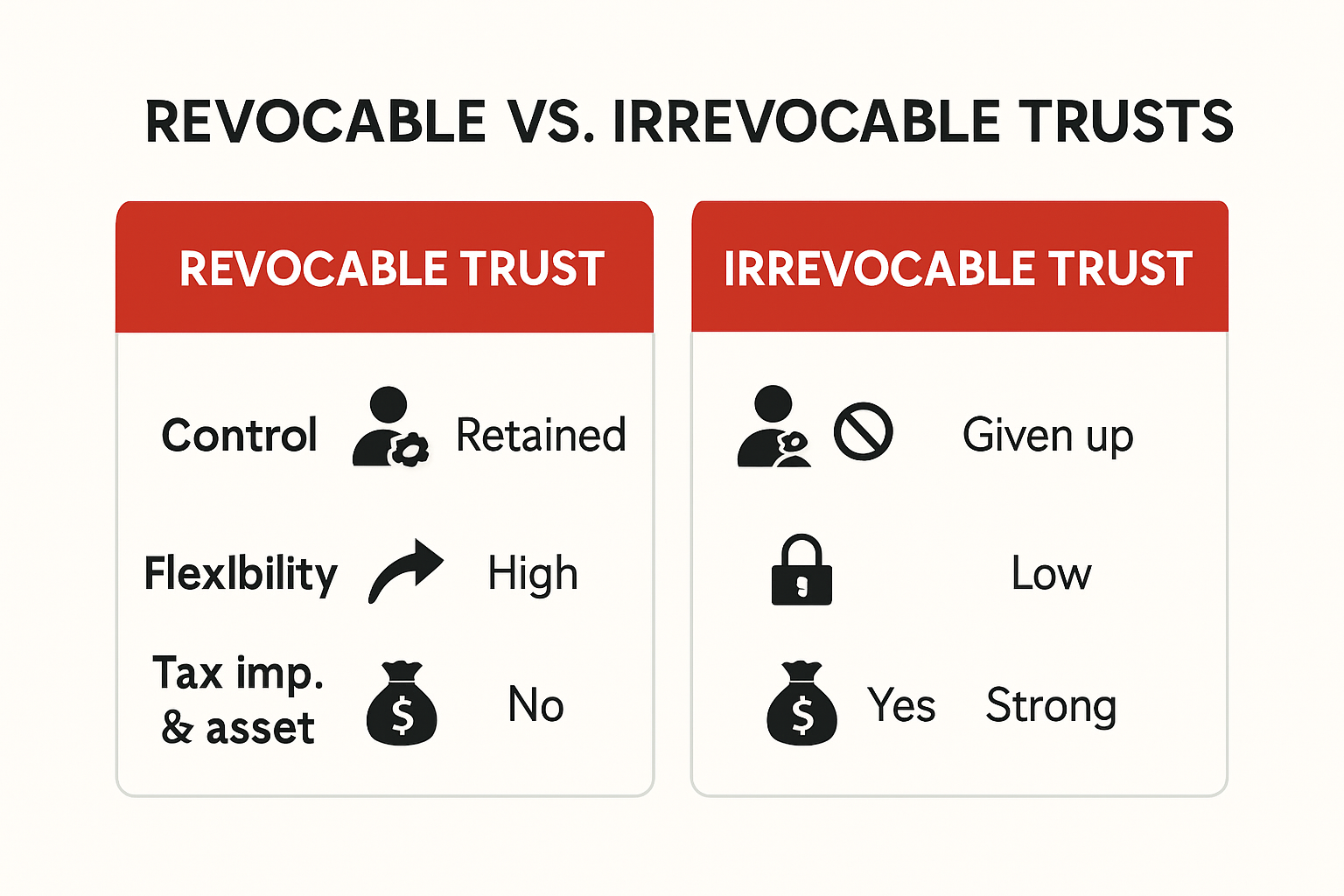

Key Differences Between Revocable and Irrevocable Trusts

Understanding the key differences between revocable and irrevocable trusts is crucial for effective estate planning. While both are legal instruments designed to manage and protect assets, they function quite differently and offer distinct advantages for families seeking comprehensive financial protection.

To help clarify the distinctions between revocable and irrevocable trusts, the following table summarizes their key features, control, tax treatment, and asset protection levels.

| Feature | Revocable Trust | Irrevocable Trust |

|---|---|---|

| Control | Grantor retains full control; can modify or dissolve anytime | Control relinquished once established; changes are difficult |

| Flexibility | Highly flexible; adapts to life changes | Rigid; limited ability to adjust |

| Tax Benefits | No immediate estate tax benefit; assets remain in taxable estate | Assets removed from taxable estate; potential estate tax savings |

| Asset Protection | Minimal protection from creditors/legal claims | Strong asset protection against most claims |

| Best For | Families seeking flexibility, young families with evolving needs | High-net-worth individuals, asset protection, advanced tax planning |

Control and Flexibility of Asset Management

The primary distinction between revocable and irrevocable trusts lies in the level of control the grantor maintains over the assets. Learn more about trust structures in our detailed estate planning guide.

Revocable trusts provide maximum flexibility. According to Cornell Law School’s Legal Information Institute, the grantor can modify, amend, or completely dissolve the trust at any time. This means you retain complete control over your assets and can make changes as your life circumstances evolve. Imagine having a financial safety net that adapts with you – that’s the power of a revocable trust.

In contrast, irrevocable trusts are significantly more rigid. Once established, these trusts cannot be easily modified without complex legal procedures or consent from all beneficiaries. The trade-off for this reduced flexibility is enhanced asset protection and potential tax benefits.

Tax Implications and Asset Protection

The tax treatment of these trusts represents another critical difference. The IRS provides clear guidance on how these trust structures are evaluated for tax purposes. Revocable trusts offer no immediate tax advantages because the assets are still considered part of the grantor’s taxable estate. The grantor continues to pay taxes on any income generated by the trust assets.

Irrevocable trusts, however, provide significant tax planning opportunities. By transferring assets out of your personal ownership, you effectively remove them from your taxable estate. This can dramatically reduce potential estate tax liabilities, protecting more of your wealth for future generations. High-net-worth families often leverage irrevocable trusts as a strategic tool to minimize tax exposure.

Asset Protection and Legal Considerations

When it comes to protecting assets from potential creditors or legal challenges, irrevocable trusts offer substantially stronger safeguards. Because you legally relinquish ownership of assets placed in an irrevocable trust, those assets are generally protected from personal legal claims, lawsuits, or bankruptcy proceedings.

Revocable trusts provide minimal asset protection since the grantor maintains ownership and control. Creditors can potentially access these assets more easily. This means if you’re in a profession with higher liability risks or concerned about potential future legal challenges, an irrevocable trust might offer more comprehensive protection.

Choosing between a revocable and irrevocable trust isn’t a one-size-fits-all decision. It requires careful consideration of your specific financial situation, long-term goals, and potential future risks. Working with an experienced estate planning attorney can help you navigate these complex options and design a trust strategy that aligns perfectly with your family’s unique needs.

Which Trust Is Right for Your California Family?

Selecting the appropriate trust for your family requires careful analysis of your unique financial landscape, long-term goals, and potential risks. Explore our comprehensive guide to California trust strategies to understand how these legal instruments can protect your family’s wealth.

Assessing Your Family’s Financial Situation

Deciding between a revocable and irrevocable trust isn’t a simple checkbox exercise. According to the University of California Office of the General Counsel, families must consider multiple factors including asset protection, tax implications, and long-term financial flexibility.

For young families with growing assets, a revocable trust often provides the most practical solution. This approach allows you to maintain complete control over your assets while creating a framework for future estate management. You can easily update beneficiaries, adjust asset allocations, and modify trust terms as your family’s needs evolve. Imagine a financial tool that grows and changes with your family – that’s the power of a revocable trust.

High-net-worth families or those with complex asset structures might find greater benefit in an irrevocable trust. By transferring assets out of personal ownership, you can potentially reduce estate tax liabilities and create a more robust asset protection strategy.

Specific Considerations for California Families

California’s unique legal landscape adds another layer of complexity to trust planning. State-specific regulations can significantly impact how trusts are structured and managed. For instance, California’s community property laws interact differently with trust strategies compared to other states.

Families with significant real estate holdings or business interests should pay special attention to trust selection. An irrevocable trust can provide enhanced protection for business assets, shielding them from personal liability and potential legal challenges. This becomes particularly crucial for entrepreneurs and professionals in high-risk industries.

Long-Term Family Wealth Protection

Beyond immediate financial considerations, the right trust can be a powerful tool for generational wealth preservation. A carefully constructed trust can provide your children with financial security while implementing guardrails that prevent potential mismanagement.

For families with minor children or concerns about heir financial responsibility, an irrevocable trust can include specific provisions that control asset distribution. This might include staggered payouts, education funding requirements, or stipulations that protect assets from potential future divorces or legal challenges.

Ultimately, there’s no one-size-fits-all solution. The most effective trust strategy requires a deep understanding of your family’s unique circumstances, financial goals, and potential future challenges. Working with an experienced estate planning attorney can help you navigate these complex decisions, ensuring that your trust not only protects your assets but also aligns with your family’s long-term vision and values.

Protecting Children and Wealth From Probate and Taxes

Protecting your children’s financial future requires strategic estate planning that goes beyond simple asset transfer. Learn how to safeguard your family’s wealth through intelligent trust strategies that minimize tax burdens and avoid costly probate processes.

Minimizing Probate Complications

Probate can be a complex, expensive, and time-consuming process that drains your family’s resources and exposes your estate to public scrutiny. According to T. Rowe Price research, placing assets in a revocable living trust can significantly reduce probate costs by allowing assets to pass directly to beneficiaries without court intervention.

Revocable trusts create a streamlined mechanism for asset transfer. By establishing a clear, legally binding framework, you can ensure your children receive their inheritance quickly and efficiently. This approach eliminates many of the delays and expenses associated with traditional probate proceedings, protecting your family from unnecessary financial and emotional stress during an already challenging time.

Strategic Tax Planning for Wealth Preservation

Tax considerations play a critical role in effective estate planning. Investopedia highlights that assets placed in an irrevocable trust are removed from the grantor’s taxable estate, potentially reducing estate tax liabilities.

For high-net-worth families, strategic tax planning can mean the difference between preserving wealth and losing a significant portion to tax obligations. Irrevocable trusts offer a powerful mechanism for minimizing tax exposure. By transferring assets out of your personal estate, you can potentially reduce or eliminate estate taxes, ensuring more of your hard-earned wealth passes directly to your children.

Advanced Protection Strategies for Life Insurance and Inheritance

Kiplinger’s expert guidance reveals the power of Irrevocable Life Insurance Trusts (ILITs) as a sophisticated estate planning tool. These specialized trusts can hold life insurance policies outside of your taxable estate, providing tax-free benefits to your beneficiaries.

ILITs create a unique layer of protection for your children. By placing life insurance policies within this trust structure, you ensure that death benefit proceeds are not included in your taxable estate. This means your children receive the full value of the life insurance policy without being diminished by estate taxes.

Each family’s financial situation is unique, requiring a personalized approach to estate planning. The most effective strategy combines multiple tools – revocable and irrevocable trusts, life insurance trusts, and careful asset positioning – to create a comprehensive protective framework.

Working with an experienced estate planning attorney allows you to navigate these complex legal mechanisms. They can help you design a trust strategy that not only minimizes tax liabilities and avoids probate but also provides clear guidelines for asset distribution, protecting your children’s financial future and preserving your family’s legacy.

Real-Life Scenarios: Avoiding Common Estate Planning Mistakes

Estate planning is a complex journey fraught with potential pitfalls that can derail your family’s financial future. Discover strategies to protect your legacy and avoid the most critical errors families make when establishing trusts.

To help you avoid common pitfalls, the following table summarizes frequent estate planning mistakes and the proactive actions that can help prevent them, based on real-life scenarios described in the article.

| Common Mistake | Potential Impact | Proactive Solution |

|---|---|---|

| Outdated Trust Documentation | Ex-spouse or unintended party may inherit assets | Review and update trust documents every 3-5 years or after major life events |

| Overestimating Revocable Trust Asset Protection | Assets remain exposed to creditors or lawsuits | Use irrevocable trusts for robust asset protection, especially for high-risk professionals |

| Poor Tax Planning | Unplanned estate taxes could diminish family wealth | Work with an experienced attorney to structure trusts for tax efficiency |

| Inadequate Asset Distribution Provisions | Heirs may mismanage or lose inheritance | Include specific payout schedules and safeguarding clauses in trusts |

The Costly Mistake of Outdated Documentation

Many families unknowingly create significant risks by failing to update their estate planning documents. Life changes rapidly – marriages, divorces, births, deaths, and significant financial shifts can render existing trust structures obsolete. A trust created five years ago might no longer reflect your current family dynamics or financial situation.

Consider the scenario of a divorced professional who neglected to update their trust after a significant life change. Their ex-spouse could potentially remain a beneficiary, inadvertently receiving assets intended for their children. This common oversight can lead to years of legal battles and emotional stress for your family.

Regular review with an estate planning attorney becomes crucial. Experts recommend comprehensive trust document reviews every three to five years or immediately after major life events. This proactive approach ensures your trust remains aligned with your current wishes and family circumstances.

Misunderstanding Asset Protection Limitations

One of the most dangerous misconceptions surrounds the protective capabilities of different trust structures. Many families mistakenly believe that simply creating a trust automatically shields their assets from all potential risks.

Revocable trusts, while flexible, offer minimal asset protection. Creditors can still access these assets since the grantor maintains control. High-risk professionals such as doctors, lawyers, and business owners must be particularly cautious. An irrevocable trust provides significantly stronger asset protection by legally transferring ownership outside of personal control.

Real-world examples illustrate these risks dramatically. A business owner who maintains all assets in a revocable trust could lose everything in a professional liability lawsuit. By contrast, strategically structured irrevocable trusts can create robust barriers against potential legal claims.

The Tax Planning Trap

Tax implications represent another critical area where families frequently make costly mistakes. Improper trust structuring can result in unexpected tax burdens that significantly diminish the wealth passed to future generations.

Many high-net-worth families fail to understand the nuanced tax treatments of different trust types. A revocable trust offers no immediate tax advantages, as assets remain part of the taxable estate. Irrevocable trusts, however, can provide substantial tax mitigation strategies when carefully designed.

Complex scenarios like multi-generational wealth transfer require sophisticated planning. A poorly structured trust might inadvertently trigger substantial estate taxes, potentially consuming a significant portion of your family’s accumulated wealth.

Navigating these intricate legal and financial landscapes demands more than basic documentation. It requires a comprehensive, forward-thinking approach that anticipates potential challenges and proactively addresses them.

Working with an experienced estate planning attorney becomes not just advisable but essential. They can help you design a trust strategy that adapts to your evolving life circumstances, provides meaningful asset protection, and minimizes potential tax liabilities. Your family’s financial legacy depends on making informed, strategic decisions today that will protect and nurture their future prosperity.

Frequently Asked Questions

What is the main difference between a revocable and irrevocable trust?

The main difference lies in control. A revocable trust allows the grantor to modify or dissolve it at any time, offering maximum flexibility. In contrast, an irrevocable trust cannot be easily changed or dissolved once established, providing stronger asset protection and tax benefits.

How does a revocable trust affect estate taxes compared to an irrevocable trust?

Revocable trusts do not provide immediate estate tax benefits because assets remain part of the grantor’s taxable estate. Irrevocable trusts, however, remove assets from the grantor’s taxable estate, potentially reducing estate tax liabilities and safeguarding wealth for future generations.

Can assets in a revocable trust be protected from creditors?

No, assets in a revocable trust offer minimal protection from creditors as the grantor retains control over these assets. In contrast, assets in an irrevocable trust are generally shielded from creditors due to the relinquishing of ownership by the grantor.

How often should I update my trust documents?

It is recommended to review and update trust documents every three to five years or after significant life events, such as marriages, divorces, or changes in financial circumstances, to ensure they align with your current family dynamics and wishes.

Take Control of Your Family’s Financial Future in California

Are you worried that choosing the wrong trust could leave your legacy vulnerable to taxes, probate, or family disputes? Many people do not realize the real difference between revocable and irrevocable trusts until it is too late. Without the right guidance, your assets could end up trapped by probate or eaten away by unnecessary costs and legal challenges—risks outlined clearly throughout our article. If securing your family’s future and avoiding hidden estate planning problems matters to you, this is the moment to act.

Explore our Wills & Trusts resources or visit our Estate Planning page for insight crafted specifically for California families. The Law Offices of Eric Ridley are dedicated to building the right trust structure for your personal situation so you can avoid probate complications and protect loved ones. Schedule your confidential consultation at https://ridleylawoffices.com today and put your estate plan on the right path—your peace of mind cannot wait.

Recommended

- Irrevocable Trust Definition: Estate Planning for California Families (2025) – Law Office of Eric Ridley

- How a Revocable Living Trust Can Protect Your Assets – Law Office of Eric Ridley

- The Benefits of a Revocable Living Trust – Law Office of Eric Ridley

- Revocable Living Trusts Explained – Law Office of Eric Ridley