PARENTS & HOMEOWNERS: MY 7-STEP ESTATE PLANNING PROCESS WILL PROTECT YOUR HEIRS

From Creditors, Predators & Bad Choices, And Will Help You Become a (Bigger) Hero to Your Family!

Non Probate Assets: 2026 Ultimate Guide

{

“@type”: “Article”,

“author”: {

“url”: “https://ridleylawoffices.com”,

“name”: “Ridley Law Offices”,

“@type”: “Organization”

},

“@context”: “https://schema.org”,

“headline”: “Understanding Non Probate Assets: Protect Your Wealth”,

“publisher”: {

“url”: “https://ridleylawoffices.com”,

“name”: “Ridley Law Offices”,

“@type”: “Organization”

},

“inLanguage”: “en”,

“articleBody”: “Delve into non probate assets to understand their importance in estate planning and protecting your family’s wealth and future.”,

“description”: “Delve into non probate assets to understand their importance in estate planning and protecting your family’s wealth and future.”,

“datePublished”: “2025-08-28T02:57:14.762Z”,

“mainEntityOfPage”: {

“@id”: “https://ridleylawoffices.com/understanding-non-probate-assets-protect-your-wealth”,

“@type”: “WebPage”

}

}

Most people think creating a will is all it takes to control who inherits their money or property when they die. Yet over $1 trillion in financial assets pass outside of probate every year in the US. That means the real power to decide where your wealth ends up often depends on non probate assets, not your will. If you want your wishes honored or your family’s inheritance protected, you’ll need to look closer at what actually skips the court system entirely.

Table of Contents

- What Are Non Probate Assets And How Do They Differ From Probate Assets?

- Why Non Probate Assets Matter In Estate Planning

- How Non Probate Assets Function During Estate Settlement

- Key Types Of Non Probate Assets And Their Implications

- Practical Considerations For Managing Non Probate Assets

Quick Summary

| Takeaway | Explanation |

|---|---|

| Non probate assets bypass probate court | These assets transfer directly to beneficiaries without entering the legal court process, ensuring quick access. |

| Beneficiary designations are crucial | Regularly update beneficiary information to ensure assets go to intended heirs and avoid conflicts. |

| Assets like life insurance expedite wealth transfer | Life insurance and retirement accounts allow for immediate transfers upon death, reducing delay and complexity. |

| Strategic asset management avoids legal complications | Proper structuring of non probate assets reduces legal fees, minimizes conflicts, and protects financial privacy. |

| Integration with estate planning can minimize taxes | Coordinating non probate assets with your overall estate plan helps in managing tax liabilities and maximizing wealth preservation. |

What Are Non Probate Assets and How Do They Differ from Probate Assets?

Non probate assets represent a crucial yet often misunderstood category of property that bypasses the traditional probate court process when transferring ownership after someone’s death. Understanding these assets can significantly impact how your wealth is distributed and protected.

Defining Non Probate Assets

Non probate assets are financial instruments and properties that transfer directly to designated beneficiaries without going through probate court. According to Cornell Law School, these assets pass by survivorship or contract rather than through a traditional will. This means the transfer happens automatically, outside of court supervision.

Key characteristics of non probate assets include:

- Direct transfer to named beneficiaries

- Bypass probate court proceedings

- Often governed by specific contractual agreements

- Typically transfer more quickly than probate assets

How Non Probate Assets Work

Non probate assets operate through specific legal mechanisms that predetermine asset distribution.

Common examples include:

- Life insurance policies with named beneficiaries

- Retirement accounts like 401(k)s and IRAs

- Jointly owned real estate with right of survivorship

- Payable on death (POD) bank accounts

- Transfer on death (TOD) investment accounts

These assets are transferred based on beneficiary designations or ownership structures established before the owner’s death. For instance, a life insurance policy pays directly to the named beneficiary, completely circumventing probate court. This means faster access to funds and reduced legal complexity for your heirs.

Why Non Probate Assets Matter

Choosing the right asset structure can protect your family’s financial future. Our guide on probate alternatives offers deeper insights into strategic estate planning. Non probate assets provide several significant advantages: they reduce legal fees, minimize potential family conflicts, accelerate asset transfer, and offer more privacy compared to traditional probate processes.

By understanding and strategically utilizing non probate assets, you can create a more efficient and streamlined approach to wealth transfer, ensuring your loved ones receive their inheritance with minimal complications.

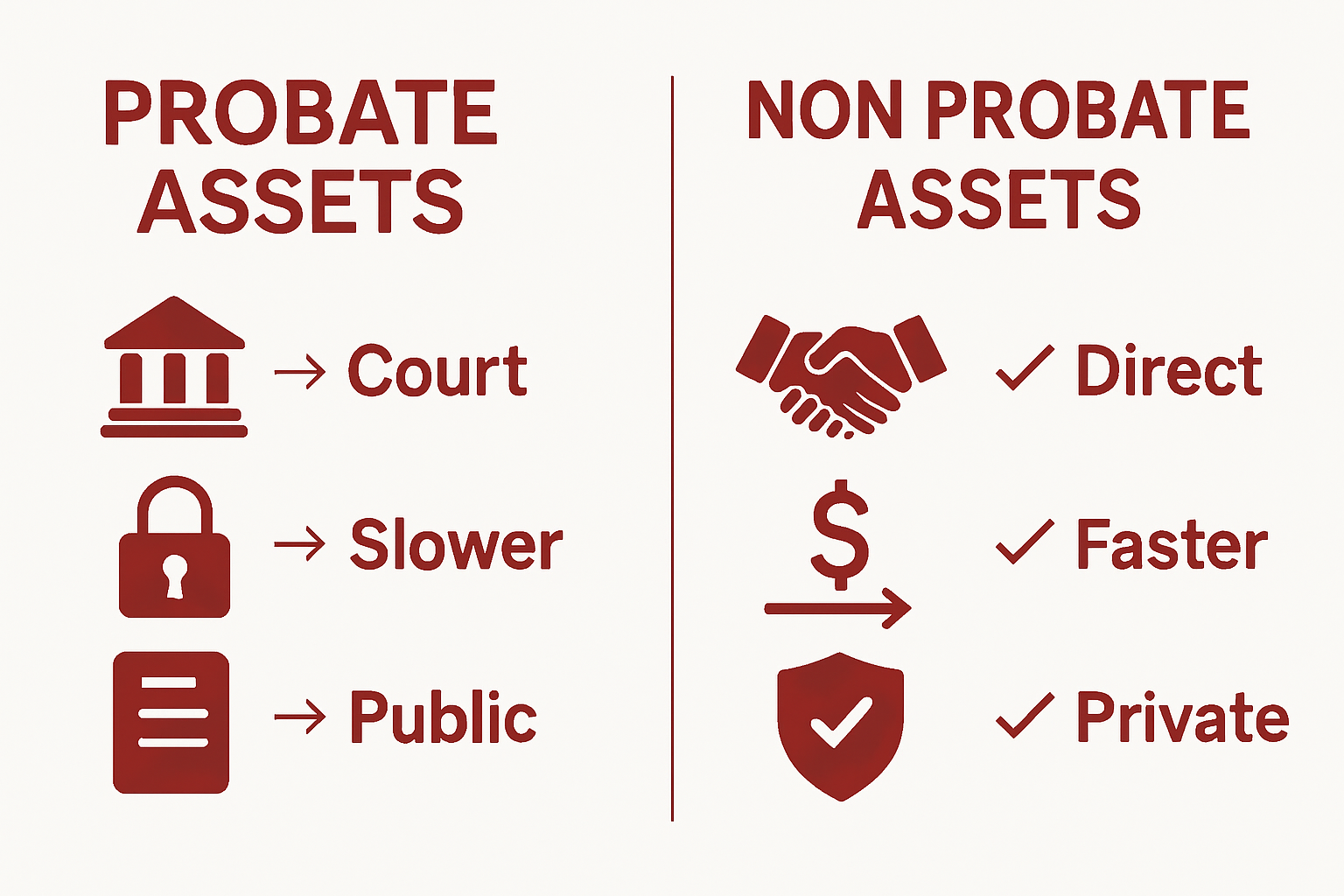

To help clarify the distinction between probate and non probate assets, the following table compares their key characteristics and implications on estate planning and wealth transfer efficiency.

| Aspect | Probate Assets | Non Probate Assets |

|---|---|---|

| Transfer Process | Goes through court-supervised probate process | Bypasses probate; transfers directly to beneficiaries |

| Speed of Inheritance | Can be slow, often months or longer | Typically faster; immediate or quick transfer |

| Public Record | Becomes part of the public record | Transfer remains private |

| Asset Examples | Individual real estate, personal property not jointly owned | Life insurance, retirement accounts, joint real estate |

| Role of Will | Distributed per the will or state law | Distributed by contract or ownership structure |

| Potential for Family Conflict | Increased due to court process and delays | Reduced due to automatic, direct transfer |

| Exposure to Legal Fees | Often higher due to court oversight | Usually lower, minimized legal intervention |

Why Non Probate Assets Matter in Estate Planning

Estate planning isn’t just about creating a will. Strategic management of non probate assets can dramatically transform how your wealth is protected and transferred to future generations. Understanding these assets provides a critical layer of financial security and family protection.

Minimizing Legal Complications

Non probate assets offer a streamlined approach to wealth transfer that reduces legal complexity. Learn how to avoid common probate pitfalls through strategic asset planning. By bypassing traditional probate court, these assets ensure:

- Faster inheritance distribution

- Reduced legal expenses

- Enhanced privacy for family financial matters

- Decreased potential for family conflicts

Financial Privacy and Efficiency

According to the Consumer Financial Protection Bureau, placing assets in mechanisms like revocable living trusts allows for private, efficient wealth transfer outside public court proceedings. This approach protects sensitive financial information and accelerates asset distribution.

Key advantages include:

- Immediate asset transfer to beneficiaries

- Protection from public record exposure

- Reduced administrative overhead

- Potential tax planning benefits

Strategic Wealth Preservation

Non probate assets are not just about transfer speed—they represent a sophisticated approach to wealth preservation. These assets can provide critical protection against potential creditors, legal challenges, and unexpected financial complications. Proper structuring ensures your intended beneficiaries receive their inheritance with minimal external interference.

By carefully designating beneficiaries, utilizing transfer mechanisms, and understanding the nuanced legal landscape, you can create a robust estate plan that transcends traditional will-based approaches. Your wealth becomes a well-protected legacy, designed to support and empower future generations with minimal bureaucratic friction.

How Non Probate Assets Function During Estate Settlement

Estate settlement involves complex legal processes where non probate assets play a critical role in efficiently transferring wealth. Understanding how these assets navigate the settlement landscape can provide significant advantages for families managing an estate.

Automatic Transfer Mechanisms

Learn the intricacies of probate in California to better comprehend non probate asset transfers. According to the Internal Revenue Service, non probate assets transfer through predetermined mechanisms that bypass traditional court proceedings.

Key transfer methods include:

- Direct beneficiary designations

- Joint ownership with right of survivorship

- Transfer on death (TOD) accounts

- Payable on death (POD) financial instruments

- Revocable living trusts

Legal and Financial Implications

Non probate assets are not completely exempt from legal scrutiny. The Uniform Nonprobate Transfers on Death Act establishes that beneficiaries might be responsible for certain estate obligations. These assets can still be subject to:

- Creditor claims against the estate

- Potential tax assessments

- Partial liability for estate settlement expenses

- Statutory allowances for surviving spouse or dependents

Settlement Process Dynamics

The settlement of non probate assets differs significantly from traditional probate assets. While probate assets go through court-supervised distribution, non probate assets transfer more directly. Beneficiaries typically receive these assets:

- Faster than traditional inheritance

- With minimal legal intervention

- Through direct financial institution transfers

- With reduced administrative complexity

By understanding these nuanced transfer mechanisms, families can strategically manage their estate settlement, ensuring smoother wealth transition and minimizing potential legal complications. Non probate assets represent a sophisticated approach to estate planning that prioritizes efficiency and direct beneficiary protection.

Key Types of Non Probate Assets and Their Implications

Navigating the landscape of non probate assets requires understanding their diverse forms and nuanced legal implications. Different asset types offer unique strategies for efficient wealth transfer and protection.

Life Insurance and Retirement Accounts

Explore alternatives to traditional probate court for comprehensive estate planning. According to Cornell Law School, life insurance and retirement accounts represent powerful non probate asset categories with significant transfer capabilities.

Key characteristics include:

- Direct beneficiary designation

- Immediate transfer upon death

- Typically tax-advantaged

- Bypassing traditional probate processes

- Potential creditor protection

Investment and Bank Accounts

Transfer on Death (TOD) and Payable on Death (POD) accounts offer strategic wealth management options. The U.S. Securities and Exchange Commission highlights that these accounts enable direct asset transfer without court intervention.

Important considerations include:

- Simplified asset transition

- Maintaining control during account holder’s lifetime

- Potential limitations on beneficiary designations

- State-specific registration requirements

- FDIC insurance implications

Real Estate and Joint Ownership

Joint ownership with right of survivorship represents another sophisticated non probate asset strategy. This approach allows property to transfer automatically upon an owner’s death, creating a seamless wealth transition mechanism.

Strategic benefits encompass:

- Immediate property transfer

- Avoiding complex probate proceedings

- Potential tax efficiency

- Simplifying inheritance process

- Maintaining family property continuity

By understanding these non probate asset types, families can develop comprehensive estate plans that prioritize efficiency, privacy, and strategic wealth preservation. Careful asset structuring transforms estate planning from a reactive legal process into a proactive wealth management strategy.

This table organizes the main types of non probate assets discussed in the article, summarizing their features and unique considerations relevant for estate planning.

| Asset Type | Primary Transfer Mechanism | Key Features | Legal/Tax Considerations |

|---|---|---|---|

| Life Insurance Policies | Beneficiary designation | Immediate payout, bypasses probate | Typically tax-advantaged, creditor protection |

| Retirement Accounts (401k, IRA) | Beneficiary designation | Direct transfer, preserves account tax status | May have income tax consequences |

| Jointly Owned Real Estate | Right of survivorship | Automatic property transfer upon death | Avoids probate, potential tax efficiency |

| Payable on Death (POD) Accounts | Named beneficiary on account | Simplified transfer, maintains owner control | FDIC insurance limits apply, state-specific rules |

| Transfer on Death (TOD) Accounts | Beneficiary registration on account | Directly passes investments, avoids court | State registration varies, potential restrictions |

| Revocable Living Trusts | Trust agreement/terms | Immediate, private asset distribution | Complex tax rules, strong privacy protections |

Practical Considerations for Managing Non Probate Assets

Effective management of non probate assets demands strategic planning, ongoing attention, and a comprehensive understanding of legal nuances. Proactive approaches can help families preserve wealth and minimize potential complications during asset transfer.

Beneficiary Designation Maintenance

Learn more about comprehensive estate planning strategies to protect your assets. According to the U.S. Supreme Court, beneficiary designations on certain assets like retirement accounts and life insurance policies take precedence over will provisions.

Critical considerations include:

- Regularly updating beneficiary information

- Reviewing designations after major life events

- Checking for potential conflicts with will provisions

- Understanding plan-specific transfer rules

- Accounting for contingent beneficiaries

Asset Coverage and Legal Protections

Understanding the scope of asset coverage and potential legal implications is crucial. Federal regulations provide complex frameworks for how non probate assets interact with various legal scenarios.

Key legal protection aspects:

- Medicaid estate recovery rules

- Federal protections for retirement accounts

- State-specific asset transfer regulations

- Potential creditor claim vulnerabilities

- Insurance and deposit account coverage limits

Tax and Financial Planning Integration

Non probate assets require sophisticated integration with broader financial and tax planning strategies. Careful management can help minimize tax liabilities and optimize wealth transfer.

Strategic planning elements include:

- Coordinating asset transfer with overall estate plan

- Understanding tax implications of different asset types

- Evaluating potential income and estate tax consequences

- Balancing liquidity needs with long-term wealth preservation

- Consulting with financial and legal professionals

By approaching non probate assets with meticulous attention and strategic foresight, families can create robust wealth transfer mechanisms that provide financial security and minimize potential legal complications.

Ready to Secure Your Non Probate Assets in California?

Understanding how non probate assets work can mean the difference between a smooth transition for your family and costly, drawn-out court proceedings. If you worry about the impact of probate delays or want to protect your loved ones from unnecessary expenses and conflicts, now is the time to act. Our Estate Planning solutions at The Law Offices of Eric Ridley address these exact challenges using proven strategies covered in this article.

Your assets deserve protection, and your family deserves peace of mind. Get trusted guidance on beneficiary designations, trust creation, and custom strategies for avoiding probate complications. Visit https://ridleylawoffices.com or explore our Wills & Trusts services to take the first step toward securing your legacy today. Don’t let uncertainty put your estate at risk. Reach out now and discover how easy professional planning can be.

Frequently Asked Questions

What are non probate assets?

Non probate assets are financial instruments and properties that transfer directly to designated beneficiaries without going through probate court, such as life insurance policies, retirement accounts, and joint real estate ownership.

How do non probate assets differ from probate assets?

Unlike probate assets, which are subject to court distribution and oversight, non probate assets bypass the probate process and transfer immediately to beneficiaries based on pre-established agreements, reducing time and legal complications.

What are some examples of non probate assets?

Common examples include life insurance policies with named beneficiaries, retirement accounts like 401(k)s and IRAs, jointly owned real estate with a right of survivorship, and payable on death (POD) bank accounts.

How can I manage my non probate assets effectively?

To manage non probate assets effectively, regularly update beneficiary designations, understand the legal implications associated with those assets, and integrate them into your overall financial and tax planning strategy.