PARENTS & HOMEOWNERS: MY 7-STEP ESTATE PLANNING PROCESS WILL PROTECT YOUR HEIRS

From Creditors, Predators & Bad Choices, And Will Help You Become a (Bigger) Hero to Your Family!

Estate Tax California 2025: Protecting Your Children’s Inheritance

More than half of American families with substantial wealth risk losing a significant portion of their legacy to complex estate tax rules each year. In California, high-net-worth parents face a unique set of challenges when planning for their children’s future because state and federal tax policies can erode inheritance faster than expected. This article reveals practical strategies to help you preserve your wealth, minimize conflict, and ensure your family’s lasting financial security.

Table of Contents

- Defining Estate Tax In California 2025

- Federal Versus State Estate Tax Rules

- Upcoming Changes And Key Exemption Thresholds

- Strategic Moves To Minimize Tax Burden

- Critical Estate Planning Mistakes To Avoid

- Trusts And Probate Avoidance For Families

Key Takeaways

| Point | Details |

|---|---|

| California Does Not Impose a State Estate Tax | Residents focus primarily on federal estate tax regulations, which can significantly impact wealth transfer strategies. |

| Federal Estate Tax Threshold is $13.99 Million in 2025 | Estates exceeding this threshold face a 40% tax rate on amounts above it, necessitating strategic planning. |

| Proposed Wealth Tax Signals Changes | A potential California wealth tax targeting billionaires could affect future estate planning strategies for high net worth families. |

| Trusts Can Enhance Estate Planning | Establishing trusts can help avoid probate and protect inherited assets, making them essential for wealth preservation. |

Defining Estate Tax In California 2025

Understanding estate tax involves comprehending the complex legal mechanism for transferring wealth after an individual’s death. In California, the estate tax landscape has unique characteristics that high net worth families must carefully navigate. Estate tax is a tax on the right to transfer property at death, calculated based on the fair market value of all possessions at the time of death.

Currently, California does not impose a separate state-level estate tax, which means residents primarily contend with federal estate tax regulations. The state eliminated its own estate tax requirement in 2005, leaving federal guidelines as the primary framework for wealth transfer taxation. This means wealthy California families must focus on federal thresholds and potential tax liabilities when planning their estate strategies.

The federal estate tax applies to estates exceeding specific value thresholds, with tax rates that can significantly impact generational wealth transfer. Assets subject to taxation include real estate, cash, business interests, investments, and other valuable possessions. Specific deductions are available, such as expenses related to estate administration, outstanding debts, and property transfers to surviving spouses or charitable organizations.

Pro tip: Consult with an estate planning professional annually to reassess your estate’s potential tax exposure and explore strategic wealth transfer mechanisms that can help minimize federal tax liabilities.

Federal Versus State Estate Tax Rules

Navigating the complex landscape of estate taxation requires understanding the critical differences between federal and California state regulations. Federal estate tax rules establish specific thresholds and rates for wealth transfer that significantly impact high net worth families. In 2025, the federal estate tax applies to estates exceeding $13.99 million, with a substantial 40% tax rate for amounts above this threshold.

California’s approach to estate taxation differs markedly from federal guidelines. The state eliminated its own estate tax program by 2005, leaving federal regulations as the primary framework for estate planning. This means California residents must focus exclusively on federal estate tax rules, which include complex provisions for spousal transfers, charitable bequests, and special considerations for small businesses and agricultural properties.

The implications of these tax rules are profound for wealthy families. While California does not impose a state-level estate tax, the federal 40% tax rate can substantially reduce the wealth transferred to heirs. Strategic estate planning becomes crucial, with techniques like lifetime gifts, establishing trusts, and careful asset structuring potentially helping to mitigate the tax burden. Families must also remain alert to potential future changes in tax legislation that could impact their long-term wealth transfer strategies.

Pro tip: Consult with a specialized estate planning attorney annually to develop a comprehensive strategy that adapts to changing federal estate tax regulations and maximizes wealth preservation for future generations.

Here’s how federal and California estate tax rules differ in 2025:

| Aspect | Federal Estate Tax | California State Estate Tax |

|---|---|---|

| Tax Threshold | $13.99 million per estate | No state-level estate tax |

| Tax Rate Above Threshold | 40% on amounts exceeding the threshold | None (state tax eliminated) |

| Deduction Options | Spousal transfers, charitable bequests, debt payments | Not applicable in 2025 |

| Potential Future Changes | Legislative risk of lower thresholds | Proposed wealth tax for ultra-high net worth individuals |

Upcoming Changes And Key Exemption Thresholds

The landscape of estate taxation is rapidly evolving, with significant implications for high net worth families in California. Federal estate tax exemption thresholds continue to play a crucial role in inheritance planning, currently set at $13.99 million for individual estates in 2025. This substantial threshold provides meaningful protection for most families, though strategic planning remains essential for those approaching or exceeding this limit.

Unexpectedly, a proposed California ballot initiative introduces a potential new wealth tax targeting individuals and trusts with assets over $1 billion. While this measure would impact only the ultra-wealthy, it signals a potential shift in state-level taxation that could have broader implications for estate planning strategies. The proposed tax would fund critical social programs including healthcare, food assistance, and education, representing a significant potential change in California’s approach to wealth redistribution.

Navigating these complex tax landscapes requires a proactive and sophisticated approach to estate planning. High net worth families must remain vigilant about potential changes in both federal and state tax regulations. Key strategies include implementing flexible trust structures, considering strategic lifetime gifts, and maintaining close communication with estate planning professionals who can provide real-time guidance on evolving tax environments. The interplay between federal exemption thresholds and potential state-level initiatives demands a dynamic and adaptive approach to wealth preservation.

Pro tip: Schedule a comprehensive estate tax review with a qualified professional at least annually to ensure your estate plan remains optimized in light of changing federal and potential state tax regulations.

Strategic Moves To Minimize Tax Burden

Navigating the complex world of estate taxation requires sophisticated strategies to protect your children’s inheritance. Federal tax regulations offer multiple approaches to minimize estate tax burdens, with sophisticated techniques that can significantly reduce potential tax liabilities. High net worth families can leverage advanced planning methods to preserve more of their hard-earned wealth for future generations.

Strategic estate planning involves multiple sophisticated techniques designed to optimize tax efficiency. These methods include establishing specialized trusts, making strategic lifetime gifts, and carefully structuring asset transfers to maximize available exemptions. Charitable contributions can also play a crucial role in reducing overall tax exposure, allowing families to support meaningful causes while simultaneously achieving tax optimization objectives. Business owners have additional opportunities through special use valuation strategies that can help minimize the taxable value of business and agricultural assets.

The most effective tax minimization strategies require a proactive and comprehensive approach. This means regularly reviewing and updating estate plans to align with changing tax regulations, understanding the nuanced interactions between federal and potential state tax initiatives, and maintaining flexibility in asset management. Utilizing the marital deduction, creating irrevocable life insurance trusts, and implementing gifting strategies can all contribute to a robust tax mitigation plan that protects your family’s financial legacy.

Pro tip: Engage a certified estate planning attorney who specializes in tax strategy to conduct a comprehensive review of your estate plan at least once every two years, ensuring your wealth preservation strategies remain cutting-edge and legally compliant.

Critical Estate Planning Mistakes To Avoid

Estate planning requires meticulous attention to detail, as even minor oversights can dramatically impact your family’s financial future. Common estate planning mistakes can result in significant unintended consequences for inheritance and tax management, potentially undermining years of careful wealth accumulation. High net worth families must approach estate planning with strategic precision and comprehensive understanding.

One of the most critical errors is failing to create or regularly update estate planning documents. Outdated wills, improperly coordinated beneficiary designations, and neglecting to account for changing tax regulations can create substantial legal and financial vulnerabilities. Business owners and individuals with complex asset portfolios must be particularly vigilant about maintaining accurate income tax returns and understanding intricate filing requirements that could potentially increase tax burdens and complicate inheritance processes.

Navigating estate planning successfully requires a proactive, forward-thinking approach. This means conducting comprehensive reviews of all asset structures, understanding complex tax implications, and creating flexible strategies that can adapt to changing family dynamics and economic environments. Key strategies include establishing robust trusts, carefully managing asset transfers, maintaining clear communication with potential heirs, and working closely with experienced estate planning professionals who can provide nuanced guidance tailored to your specific financial landscape.

Pro tip: Schedule a comprehensive estate planning review with a qualified attorney every two to three years, or immediately after significant life events like marriages, divorces, births, or substantial changes in financial status.

Summary of common estate planning mistakes and their possible impacts:

| Mistake Type | Business Impact | Recommended Solution |

|---|---|---|

| Failing to update documents | Unexpected inheritance disputes | Review estate plan every 2-3 years |

| Outdated beneficiary designations | Incorrect asset transfer to heirs | Coordinate designations with current plan |

| Neglecting tax law changes | Increased estate tax liabilities | Consult professionals after major changes |

| Incomplete asset review | Overlooked assets increase risk | Conduct full asset inventory regularly |

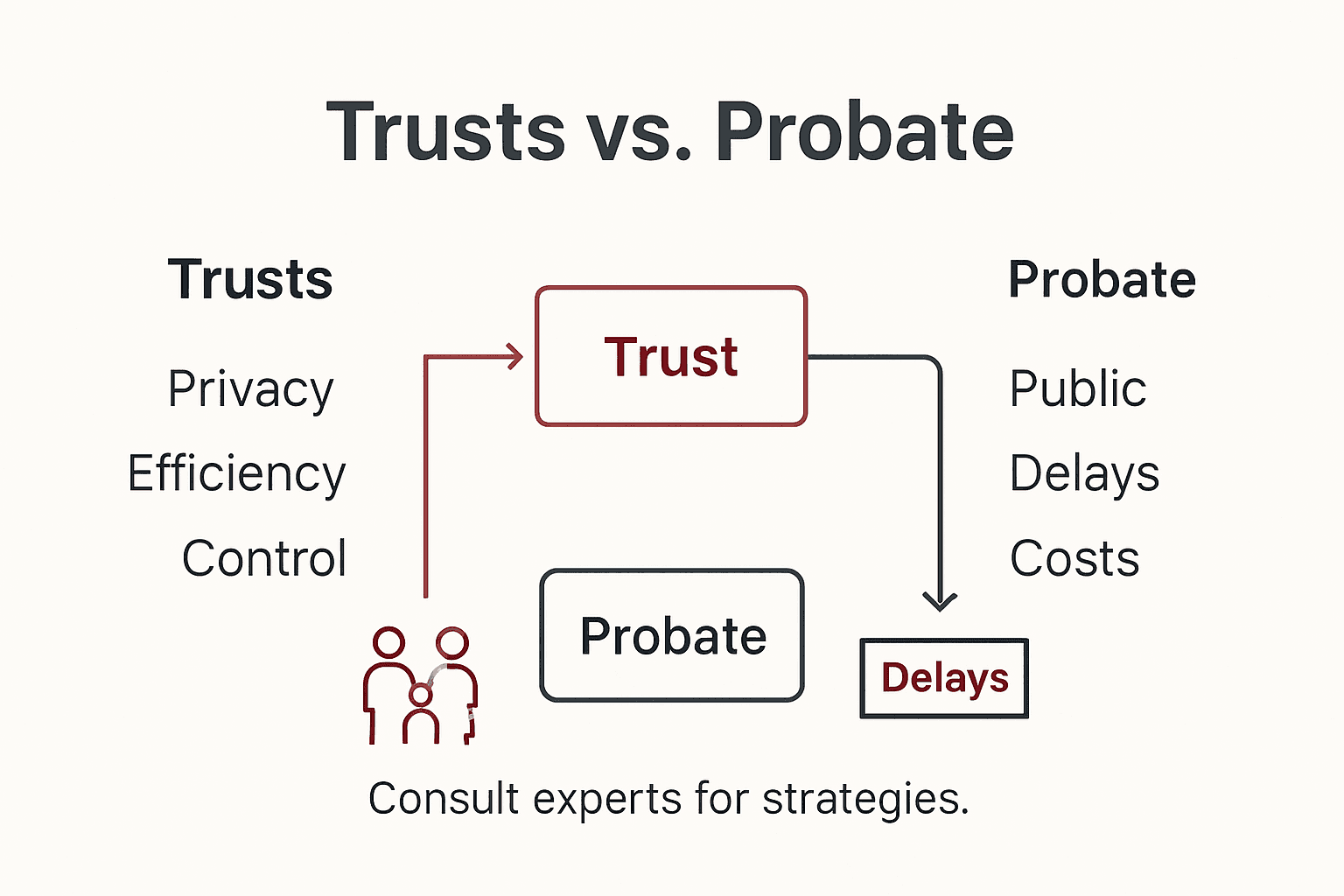

Trusts And Probate Avoidance For Families

Trusts represent a powerful estate planning tool that can dramatically transform how families protect and transfer wealth across generations. Revocable living trusts provide families with a strategic mechanism to avoid probate court proceedings, enabling direct property transfers to heirs while maintaining privacy and reducing administrative complexities. These legal instruments offer high net worth families unprecedented control over asset management and inheritance strategies.

The primary advantages of establishing trusts extend far beyond simple asset transfer. Trust administration involves sophisticated strategies for filing returns and managing distributions, ensuring compliance with California tax regulations while optimizing potential tax benefits. By carefully structuring trusts, families can protect inherited assets from potential creditors, maintain flexibility in asset management, and create customized inheritance plans that reflect their unique financial goals and family dynamics.

Successful trust implementation requires a nuanced understanding of legal and financial landscapes. Different trust structures offer varying levels of protection and control, including revocable and irrevocable trusts, generation-skipping trusts, and specialized vehicles designed for specific asset types. Families must work closely with experienced estate planning professionals to develop comprehensive strategies that adapt to changing tax laws, family circumstances, and long-term wealth preservation objectives.

Pro tip: Consult with an estate planning attorney specializing in trust creation to develop a personalized strategy that aligns with your family’s specific financial landscape and inheritance goals.

Secure Your Family’s Legacy Against California Estate Tax Challenges in 2025

The upcoming changes in estate tax regulations present real challenges for protecting your children’s inheritance in California. With federal estate tax thresholds, potential new wealth taxes, and complex trust strategies, you need expert guidance to avoid costly mistakes and preserve your family wealth. Understanding terms like trusts, probate avoidance, and strategic lifetime gifts is essential, but navigating these options alone can feel overwhelming.

Take control today by partnering with trusted advisors who focus exclusively on estate planning and probate. Explore comprehensive solutions at Estate Planning – Law Office of Eric Ridley and deepen your understanding by reviewing Wills & Trusts – Law Office of Eric Ridley.

Don’t let changing tax laws erode your family’s legacy. Visit The Law Offices of Eric Ridley now to secure a personalized estate plan that minimizes taxes, avoids probate delays, and protects what matters most. Act now to safeguard your children’s future before 2025 brings new regulations that could impact your estate.

Frequently Asked Questions

What is the estate tax threshold for 2025?

The federal estate tax threshold for 2025 is set at $13.99 million for individual estates, meaning estates valued below this amount are not subject to federal estate tax.

Does California have a state estate tax in 2025?

No, California does not impose a separate state estate tax as it eliminated its estate tax requirement in 2005, meaning residents only need to consider federal estate tax regulations.

What are some strategies to minimize estate tax burdens?

Effective strategies include establishing trusts, making lifetime gifts, and utilizing charitable contributions. These methods help reduce taxable estates and preserve wealth for future generations.

How can trusts help avoid probate?

Revocable living trusts enable direct transfers of assets to heirs, thereby avoiding probate court proceedings. This not only maintains privacy but also reduces administrative complexities.

Recommended

- California Estate Tax Planning 2025: Protecting Your Family’s Wealth – Law Office of Eric Ridley

- Estate Planning for Parents in California: Protecting Wealth in 2025 – Law Office of Eric Ridley

- Estate Planning Checklist 2025: Protecting California Families – Law Office of Eric Ridley

- Family Legacy Planning in California: Secure Your Wealth for 2025 – Law Office of Eric Ridley

- Exiting Wealthy is Not in the Endgame – It’s in the Everyday – Summit Scale