PARENTS & HOMEOWNERS: MY 7-STEP ESTATE PLANNING PROCESS WILL PROTECT YOUR HEIRS

From Creditors, Predators & Bad Choices, And Will Help You Become a (Bigger) Hero to Your Family!

What Is a Living Trust? Complete Guide for California

{

“@type”: “Article”,

“author”: {

“url”: “https://ridleylawoffices.com”,

“name”: “Ridleylawoffices”,

“@type”: “Organization”

},

“@context”: “https://schema.org”,

“headline”: “What Is a Living Trust? Complete Guide for California”,

“publisher”: {

“url”: “https://ridleylawoffices.com”,

“name”: “Ridleylawoffices”,

“@type”: “Organization”

},

“inLanguage”: “en”,

“description”: “What is a living trust? This comprehensive guide for California covers types, key benefits, legal requirements, funding, and living trust vs. will comparisons.”,

“datePublished”: “2025-11-08T00:13:09.139Z”

}

More than 50 percent of California estates face delays and legal fees because they lack effective trust planning. Choosing the right legal tools can make a world of difference for your family’s financial future. Whether you are looking to protect your assets, maintain privacy, or avoid probate stress, understanding how a living trust works under California law helps you stay in control and keep your wishes clear.

Table of Contents

- Defining A Living Trust In California Law

- Types Of Living Trusts And Key Differences

- How Living Trusts Work For Families

- Legal Requirements And Common Missteps

- Costs, Taxes, And Living Trust Alternatives

Key Takeaways

| Point | Details |

|---|---|

| Living Trust Benefits | A living trust provides immediate asset management, avoids probate, and enhances privacy and control over asset distribution. |

| Revocable vs. Irrevocable Trusts | Revocable trusts offer flexibility, allowing changes during the grantor’s lifetime, while irrevocable trusts provide stronger asset protection and potential tax benefits. |

| Legal Requirements | Properly funding the trust and designating beneficiaries are essential to its effectiveness; neglecting updates can compromise your estate plan. |

| Cost Considerations | Initial setup costs for a living trust range from $1,500 to $3,500, and while there is no California estate tax, federal taxes may apply based on your estate’s value. |

Defining a Living Trust in California Law

A living trust is a powerful legal instrument that allows you to protect and manage your assets during your lifetime and beyond. According to Santa Clara Courts, a living trust is a legal tool for financial planning where a person (Trustee) can hold another person’s (Settlor’s) property for the benefit of someone else (Beneficiary).

Unlike a traditional will, a living trust goes into effect immediately during your lifetime. As California Attorney General’s Office explains, this legal document enables you to place your assets into a trust with specific instructions for their management and distribution upon your death or potential incapacity. This means you maintain control over your assets while creating a flexible mechanism for future asset transfer.

Key characteristics of a living trust in California include:

- Assets remain under your direct control during your lifetime

- Provides seamless asset management if you become incapacitated

- Helps your estate avoid the costly and time-consuming probate process

- Offers privacy since trust documents are not public record

- Allows for more complex and personalized asset distribution strategies

By establishing a living trust, California residents gain significant advantages in estate planning. You’re essentially creating a legal framework that protects your assets, provides for your loved ones, and ensures your financial wishes are honored precisely as you intend. The Role of a Living Trust in California Estate Planning can provide more detailed insights into how these legal instruments work specifically in our state.

Types of Living Trusts and Key Differences

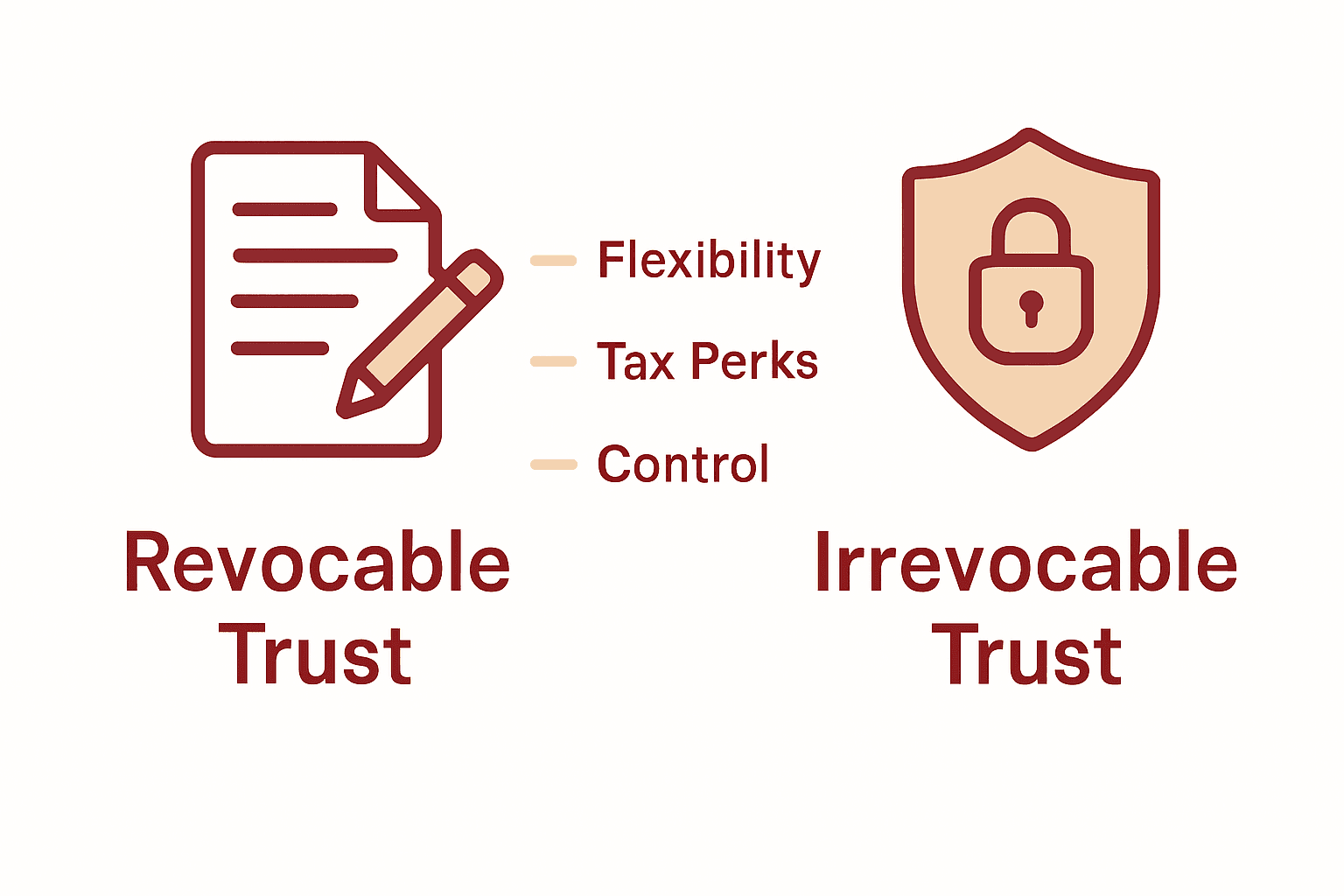

Living trusts in California come in several distinct variations, each designed to address different estate planning needs. According to SmartAsset, California law recognizes two primary types of living trusts: revocable and irrevocable trusts, each offering unique advantages and limitations for asset management and protection.

A revocable living trust provides maximum flexibility for the grantor. As Santa Clara Courts explains, these trusts can be altered or terminated by the settlor during their lifetime. This means you can modify asset distributions, add or remove property, and even completely dissolve the trust if your financial circumstances or wishes change.

Key differences between trust types include:

-

Revocable Trusts:

- Can be modified at any time

- Provides flexibility in asset management

- Assets remain under grantor’s direct control

- No immediate tax benefits

-

Irrevocable Trusts:

- Cannot be easily changed once established

- Offers potential tax advantages

- Provides stronger asset protection

- Assets transfer out of personal ownership

For families seeking comprehensive estate planning, understanding these nuanced differences is crucial. Types of Trusts in California: Protecting Family Wealth in 2025 can provide deeper insights into how different trust structures might align with your specific financial goals and family needs.

How Living Trusts Work for Families

Living trusts offer California families a powerful tool for comprehensive estate management and asset protection. According to Santa Clara Courts, a living trust allows families to manage and distribute assets without the complex probate process, ensuring a smoother transition of property to beneficiaries while maintaining complete privacy.

The mechanics of a living trust involve three primary roles: the grantor (who creates the trust), the trustee (who manages the assets), and the beneficiaries (who receive the assets). As California Attorney General’s Office explains, these trusts enable families to manage assets during the grantor’s potential incapacity and ensure precise asset distribution according to the grantor’s specific wishes upon death.

Key operational aspects of living trusts for families include:

- Immediate asset management if the grantor becomes incapacitated

- Seamless transfer of assets without court intervention

- Preservation of family wealth across generations

- Protection of assets from potential legal claims

- Customizable distribution strategies for different beneficiaries

For families navigating complex financial landscapes, understanding these nuanced mechanisms is crucial. Revocable Living Trusts for Families in California 2025 can provide deeper insights into how these legal instruments can be tailored to protect your family’s unique financial interests and legacy.

Legal Requirements and Common Missteps

Creating a living trust in California involves navigating specific legal requirements that can easily trip up unprepared individuals. According to SmartAsset, California law mandates that trusts have clearly defined beneficiaries and trustees, with assets formally transferred into the trust to ensure its effectiveness.

The legal landscape of living trusts is complex, with numerous potential pitfalls that can compromise your estate planning goals. As California Attorney General’s Office warns, common missteps include not properly funding the trust, failing to update it with life changes, and misunderstanding that a living trust does not automatically protect assets from creditors during the grantor’s lifetime.

Key legal requirements and common mistakes to avoid include:

-

Precise Beneficiary Designation

- Clearly identify all intended beneficiaries

- Use full legal names

- Specify exact asset distributions

-

Critical Trust Funding Mistakes

- Failing to transfer all intended assets into the trust

- Leaving assets outside of trust coverage

- Not updating asset listings regularly

-

Oversight and Maintenance

- Neglecting to update trust after major life events

- Failing to review beneficiary designations

- Ignoring changes in tax laws or family circumstances

The Pitfalls of DIY Trusts: Why Self-Prepared Trusts Often Fail in California offers crucial insights for those looking to avoid the most common legal missteps in trust creation. Professional guidance can help you navigate these complex requirements and protect your family’s financial future.

Costs, Taxes, and Living Trust Alternatives

Navigating the financial landscape of estate planning requires careful consideration of costs, tax implications, and available alternatives. According to SmartAsset, while California does not impose a state estate tax, federal estate taxes may still apply, making the selection of the right estate planning tool crucial for preserving your family’s wealth.

The financial investment of creating a living trust involves several components. As California Attorney General’s Office explains, potential expenses include initial attorney fees, administrative costs, and ongoing maintenance expenses. These costs can vary significantly depending on the complexity of your estate and the specific legal guidance required.

Key financial considerations and alternatives include:

-

Living Trust Costs

- Initial attorney setup fees: $1,500 – $3,500

- Annual maintenance expenses

- Potential administrative management costs

-

Alternative Estate Planning Options

- Wills: Lower initial cost, but more expensive probate process

- Joint Tenancy: No direct setup costs, but limited flexibility

- Transfer-on-Death Deeds: Minimal cost, restricted asset coverage

-

Tax Implications

- No California state estate tax

- Potential federal estate tax considerations

- Possible capital gains tax benefits

How Taxes Affect Your Estate Plan provides deeper insights into the complex tax landscape surrounding estate planning, helping you make informed decisions that maximize your family’s financial protection.

Secure Your Family’s Future with Expert Living Trust Guidance

Facing the challenge of creating a living trust can feel overwhelming. The complexities of revocable and irrevocable trusts, the need to avoid probate delays, and the importance of clear beneficiary designations all demand professional attention. You want to protect your assets and ensure your wishes are honored without costly mistakes or family conflict.

At the Law Offices of Eric Ridley, we specialize exclusively in estate planning and probate services to guide California families through these challenges with confidence. Our deep knowledge of Wills & Trusts – Law Office of Eric Ridley means you get personalized trust creation and will drafting that align perfectly with your goals.

Don’t wait until it’s too late to secure your legacy. Visit our main site at https://ridleylawoffices.com to learn how our focused estate planning solutions can help you avoid probate delays and protect your family’s future. Start with our comprehensive Estate Planning – Law Office of Eric Ridley resources and take control of your financial legacy today.

Frequently Asked Questions

What is a living trust?

A living trust is a legal document that allows a person to manage and distribute their assets during their lifetime and after their death, while avoiding the probate process.

What are the key benefits of establishing a living trust?

The main benefits of a living trust include avoiding probate, maintaining privacy, seamless asset management if the grantor becomes incapacitated, and offering flexible distribution strategies for beneficiaries.

What is the difference between a revocable and an irrevocable living trust?

A revocable living trust can be changed or terminated by the grantor at any time, offering maximum flexibility. An irrevocable living trust, on the other hand, cannot be easily modified and may provide tax advantages and better asset protection.

What are common mistakes to avoid when creating a living trust?

Common mistakes include failing to fund the trust correctly, not updating it after major life changes, and neglecting precise beneficiary designations.

Recommended

- Why Make a Living Trust: Complete California Guide

- Revocable Living Trusts for Families in California 2025 – Law Office of Eric Ridley

- The Role of a Living Trust in California Estate Planning – Law Office of Eric Ridley

- Living Trust vs Will in California: 2025 Guide for Families – Law Office of Eric Ridley